The private equity investment landscape is quickly changing, influenced by different investment strategies, regulatory reforms, and macroeconomic factors. The trends of sector specialization, co-investments, ESG integration, and alternative deal structures are reshaping the way capital gets deployed, as companies seek to adopt behaviors in response to changing market conditions. On one side, deal-making around the globe is witnessing strong activity; but rising interest rates and scrutiny out of regulators may impact the investment decisions.

Evolving Strategies in Private Equity Investment

Private equity investment is continuously adapting to the changes in the market, changing investor perspectives, and regulatory changes. Larger trends characterize these changes: changing investment tactics, further co-investments, ESG integration, and sector specialization.

Growth Equity, Buyouts & Secondary Markets

Growth equity is still the garnish that draws investors on the lookout for opportunities to cash in on fast-growing sectors, especially technology and healthcare. Buyout activity, the traditional star of private equity, is under pressure owing to changing market conditions. Several investment strategies in secondaries have become quite attractive for investors unable to manage liquidity due to new fund structures in place in reaction to varying financial markets.

ESG & Impact Investing on the Rise

Sustainability and responsible investing have settled within the integrated framework of private equity investment strategies for a long time, as firms incorporate ESG principles into their investment frameworks. These days, several investors prefer funds based on sustainability targets and demand private equity firms create impact-oriented portfolios. Besides, various regulatory bodies are taking steps to strengthen ESG disclosures and compliance rules, thus forcing operators to integrate environmental, social, and governance factors into their investment processes more stringently.

Sector-Specific vs. Generalist Funds

Sector-dedicated funds are gaining increasing acceptance for their in-depth industry knowledge which, in turn, can translate into superior results regarding investment in technology, health care, and financial services. Whereas diversified funds are critical for risk balancing, a major share of investors is clearly going for a move toward specialization itself for higher returns and some still competitive edge.

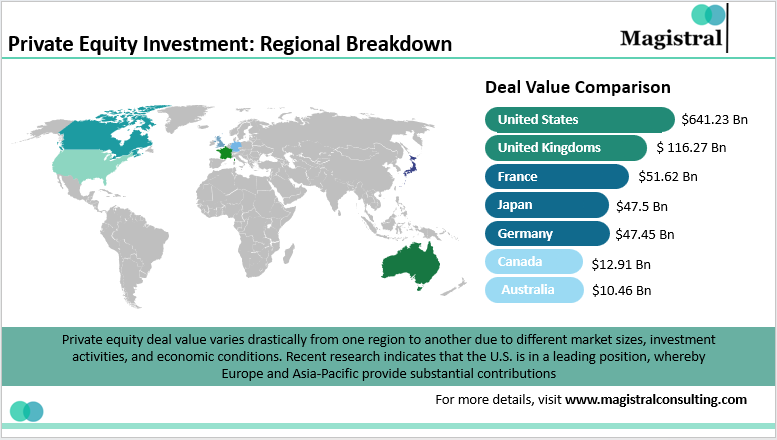

Private Equity Investment: Regional Breakdown

Private equity deal value varies drastically from one region to another due to different market sizes, investment activities, and economic conditions. Recent research indicates that the U.S. is in a leading position, whereby Europe and Asia-Pacific provide substantial contributions within the private equity investment landscape.

Private Equity Investment: Regional Breakdown

The United States Leads the Market

The U.S. remains the largest private equity market, with a total deal value of $641.23 billion. A healthy financial ecosystem, concentrated with private equity firms, along with strong corporate M&A activity, continues to attract both domestic and international investors seeking high-value opportunities.

United Kingdom: Europe’s Private Equity Hub

The UK ranks second worldwide in private equity deal value, with a total of $116.27 billion. It remains a prominent player in European deal-making activities, powered by London’s status as an international financial center with large inflows of investments, notwithstanding all the surrounding economic uncertainties.

France, Japan, and Germany: Mid-Sized Markets

In France, strong private equity activities in industrials, technology, and consumer sectors brought total deals to $51.62 billion, closely followed by Japan at $47.5 billion that benefited from corporate restructuring and broader interest among international private equity funds. Thus, even at $47.45 billion of deals, Germany retains its position as one of Europe’s largest markets, of course concentrated in manufacturing and technology investment fields.

Canada and Australia: An Emerging but Smaller Market

Private equity deals were valued in Canada at $12.91 billion largely for energy, technology, and infrastructure investment. Either way, Australia is shown to have attracted investments amounting to $10.46 billion last year, reinforcing the visibility of investors toward renewable energy, real estate, and financial services.

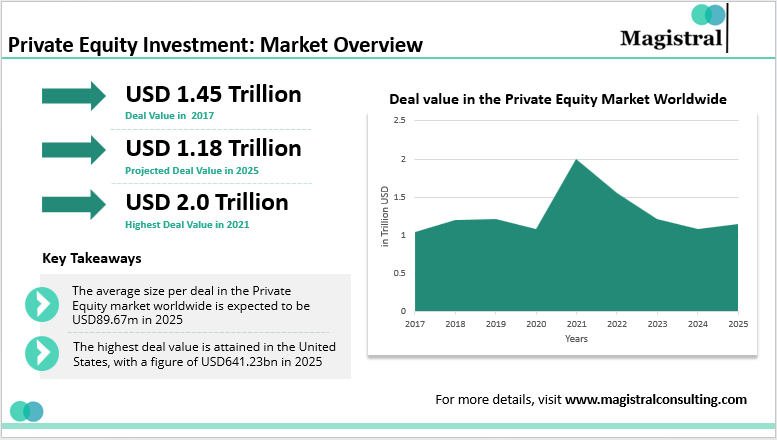

Private Equity Investment: Market Overview

Interpolated, quickly fluctuating private equity investment markets can see varying degrees of deal size change, or transaction volume as influenced by macroeconomic conditions, perceptions of investors, and real-economy sector developments.

Private Equity Investment: Market Overview

Trends in Private Equity Deal Size

The deal value is expected to reach USD 1.18 Trillion in 2025 from USD 1.45 Trillion in 2017 and the highest deal value obtained in 2021 at USD 2.0 Trillion. The average size of private equity deals has undergone fluctuations owing to business cycles and investor confidence. In 2017, the average deal was pegged at US$ 91.49 million and peaked in 2021 at US$ 116.70 million. It was due to the strong post-pandemic recovery and ample availability of capital. However, the mean deal size is expected to decline to US$ 89.50 million by 2025, primarily because of market adjustments, high interest rates, and a conservative mindset with regard to investment. This modest change leans in the direction of smaller, strategic deals as opposed to more significant leveraged buyout activity.

Number of Private Equity Deals

The volume of private equity transactions has themselves been subject to considerable swings. The number of deals rose from 2017 to 2019, with an annual count attaining a peak of $12.10 million deals by 2019. 2021 was inundated with hurricanes into the transaction volume to a record high of 17.16 million, fueled by push-pull investment activity for pandemic recovery. Deal volume fell to $10.25 million in 2024, as concerns about global economic breakdowns, increased interest rates, and geopolitics began building up. Deal volume forecasts for April 2025 again anticipate a rise to $12.87 million deals, indicating a possible improvement in market conditions.

Key Takeaways

The private equity arena remains dynamic with fluctuating deal sizes and volume once again responding to the outside world of economic and policy factors. The inclination to break down into smaller however high-potential deals is being increasingly favored over much larger high-flying, high-risk transactions. Following 2024, a disconnect sets in; a moderate yet cautious recovery set for 2025 calls for a flexible and adaptive approach to that investing climate.

Key Regulatory Shifts Impacting Private Equity

Governments around the globe are strengthening regulation over private market transactions, with an eye to investor protection and competition. The EU’s AIFMD II imposes more stringent reporting and fund advertising rules, while the U.S. SEC has implemented disclosure and fee regulations that augment compliance burdens.

Antitrust Scrutiny in Mega-Deals

Large PE deals are under close scrutiny from regulators to stop anti-competitive market dominance. The U.S. DOJ and FTC have been increasing enforcement activity, especially in healthcare, tech, and consumer markets. The European Commission too is strengthening monitoring of PE-led consolidations, affecting club deals and roll-up strategies in industry clusters.

SEC’s Push for Greater Transparency

The U.S. SEC is now requiring higher-quality disclosures around fees, performance data, and investor rights. PE firms need to give concise breakouts for carried interest and management fees. They also need to report preferential treatment in side letters, and follow more rigid quarterly performance report standards.

Taxation Considerations and Structuring Optimizations

Governments are re-examining carried interest taxation, which could raise fund manager tax liabilities. OECD’s BEPS guidelines impact investment structuring to avoid tax evasion. Moreover, fund domiciliation in tax-haven jurisdictions such as the Cayman Islands and Luxembourg is under increased scrutiny.

Magistral Consulting’s Services for Private Equity Investment

Magistral Consulting offers services for private equity investment and advises private equity firms throughout the investment life cycle, optimizing deal flow, due diligence, fundraising, and portfolio management.

Deal Origination & Market Intelligence

We assist private equity investment decisions by finding high-potential investments by screening targets, conducting market research, and competitive landscaping. Our ESG and impact investment reporting ensures compliance with evolving sustainability expectations.

Due Diligence & Investment Analysis

We conduct financial and operating due diligence, company benchmarking, and investment memorandums. We create advanced financial models, including DCF and LBO, for correct valuations and risk analysis to support private equity investments.

Fundraising & Investor Relations

Magistral assists in preparing Private Placement Memorandums, pitch decks, and investor outreach strategies. We manage investor databases, CRM systems, and communications to enhance engagement.

Portfolio Management & Value Creation

Our services include CFO outsourcing, financial reporting, and compliance support. Our expertise in cost optimization, M&A advisory, and exit planning helps PE firms maximize portfolio value.

About Magistral Consulting

Magistral Consulting has helped multiple funds and companies in outsourcing operations activities. It has service offerings for Private Equity, Venture Capital, Family Offices, Investment Banks, Asset Managers, Hedge Funds, Financial Consultants, Real Estate, REITs, RE funds, Corporates, and Portfolio companies. Its functional expertise is around Deal origination, Deal Execution, Due Diligence, Financial Modelling, Portfolio Management, and Equity Research

For setting up an appointment with a Magistral representative visit www.magistralconsulting.com/contact

About the Author

The article is authored by the Marketing Department of Magistral Consulting. For any business inquiries, you can reach out to prabhash.choudhary@magistralconsulting.com

What are the projected trends for private equity in 2025?

Key trends shaping private equity in 2025 include:

- Sustainable Investments – ESG-focused funds and impact investing.

- Sector-Specific Strategies – Preference for high-growth sectors like tech, healthcare, and fintech.

- Alternative Deal Structures – More co-investments, club deals, and secondary transactions for capital flexibility.

Which regions dominate the private equity market?

- United States – The largest PE market with $641.23 billion in deals.

- United Kingdom – Europe’s top PE hub, with $116.27 billion in transactions.

- France, Germany, Japan – Mid-sized PE markets with strong activity in industrials, technology, and consumer sectors.

- Canada & Australia – Emerging PE markets focusing on energy, tech, and infrastructure.

How is private equity deal size evolving?

- The average deal size peaked at $116.7M in 2021 due to post-pandemic capital inflows.

- A decline to $89.5M by 2025 is expected, reflecting cautious investment strategies and higher interest rates.

- Private equity deal volume is set to recover, reaching 12,870 transactions in 2025, signaling investor confidence.

What are the major regulatory challenges in private equity?

- Antitrust Scrutiny – Large PE acquisitions are under DOJ and FTC review to prevent monopolistic behavior.

- SEC Transparency Rules – Increased disclosure on management fees, carried interest, and investor rights.

- Tax Reforms – Global tax reforms such as OECD’s BEPS guidelines impact fund structuring and tax compliance.