In today’s highly competitive financial services sector, loan origination outsourcing has turned out to be an imperative strategy to improve efficiency, speed up its processes, save costs, reduce risk, and make compliance easier. The advantages of outsourcing would benefit financial institutions in terms of operational synergies, capacity within specialized skills, and concentration on core business functions.

This article talks about the primary benefits of loan origination outsourcing, which industries benefit most, and how outsourcing allows lenders to utilize better processes in ensuring quicker approvals and better compliance.

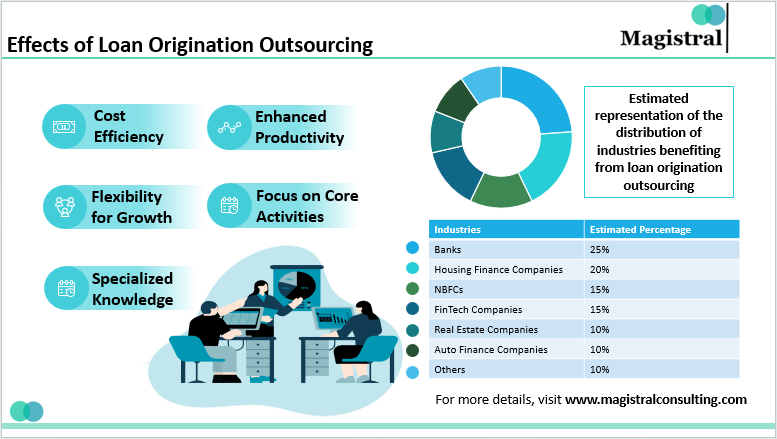

Effect of Loan Origination Outsourcing

There are a variety of effects of loan origination outsourcing and why the lender might wish to outsource their loan origination process:

Effects of Loan Origination Outsourcing

Cost Efficiency

LOS management outsourcing is far more cost-effective than having in-house personnel. External vendors take advantage of economies of scale to provide reduced pricing.

Enhanced Productivity

Outsourcing partners usually have tools and expertise to optimize LOS systems operational efficiency and streamline operations.

Access to Specialized Knowledge

Lenders tend to lack the in-house ability to manage their LOS facilities to greatest advantage. Outsourcing can not only mobilize specialized skills and experience. But can also provide lenders with the best possible opportunities for exploiting the advantages of their LOS.

Flexibility for Growth

Scalable by external providers, lenders may vary their LOS operations per demand, which is especially beneficial for organizations that undergo a seasonal variation in loan volume.

Focus on core activities

By focusing on core business functions, a lender can outsource the administration of its LOS, thus diverting its resources toward loan underwriting and servicing and away from managing systems.

Industries Benefiting from Loan Origination Outsourcing

Most industries see benefits in loan origination outsourcing because of cost savings, efficiency increases, and enhanced compliance. An estimated 25% OF banks, 20% of housing finance companies, and 15% of NBFCs already outsource for the management of high volumes of loans and underwriting and other processes. FinTech companies also save time as their processing with regard to loan applications can be hastened due to digital application outsourcing for approval. For instance, outsourcing is very useful for the acceleration and enhancing the loan disbursal of real estate and auto finance companies. The lenders to small businesses reduce costs when outsourcing loan evaluation and documentation, private equity firms as well as insurance companies who rely on due diligence and underwriting through outsourcing ensure that it works efficiently, within legal bounds.

Regulations and Compliance for Loan Origination

The following are the major regulations and compliance requirements involved in loan origination.

Key Regulations in Loan Origination Outsourcing

Truth in Lending Act (1968) (TILA)

TILA ensures that consumers receive clear, standardized information about the terms and costs of credit. TILA guidelines must be followed by a third-party loan origination service provider, thereby making the finance charges, annual percentage rates, and other information about the loan transparent to consumers. This transparency is important in gaining consumer trust.

Equal Credit Opportunity Act (1974) ECOA

ECOA prohibits discrimination on the basis of race, color, religion, national origin, sex, marital status, age, or receipt of public assistance. In loan origination outsourcing, it is significant that service providers ensure that the credit evaluation shall be fair and unbiased, in order to equally distribute credit to the people.

Real Estate Settlement Procedures Act (1974) (RESPA)

RESPA mandates that lenders disclose all settlement costs in real estate transactions. When outsourcing loan origination, it is critical for the third-party provider to comply with RESPA’s disclosure requirements, ensuring that borrowers receive transparent information about all costs involved in the loan process.

Compliance Requirements in Loan Origination Outsourcing

Know Your Customer (KYC)

Strict KYC procedures are also required to identify customers when outsourcing loan origination. Lenders must check how the third parties they would be outsourcing to are maintaining robust systems for collecting and authenticating personal information, thus helping prevent fraud and ensuring compliance with financial regulations.

Anti-Money Laundering (AML)

AML regulations necessitate monitoring and reporting suspicious activities. If the loan origination is outsourced, the third-party provider must have in place processes and procedures to identify and report any suspected activities involving money laundering so as to keep the lender’s operation compliant with relevant laws.

Data Privacy Laws

This is the EU’s GDPR and California’s CCPA on data protection regulation, which calls for proper handling of personal customer data. In this regard, these data privacy laws must be followed by third-party outsourcing firms in order to keep sensitive customer information confidential and protected while in the process of loan origination.

Future Trends

Following are some of the major future trends for the loan origination market.

Rise of Non-Banking Financial Companies (NBFCs) and FinTechs

The rise of the NBFC and FinTech concerned with the disbursement of loans has created more competition in loan origination. NBFCs and FinTech companies have introduced technology and different innovative loans, thus challenged the traditional banks and making them innovate and diversify.

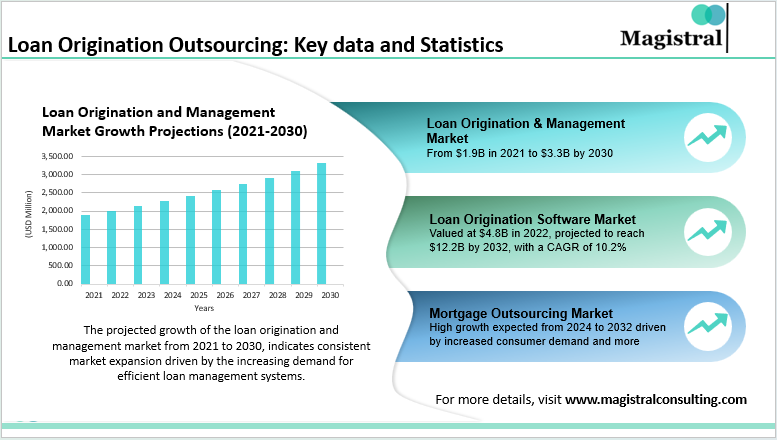

Growth in Loan Origination Software Market

The broad loan origination software segment is expected to grow to around $9 billion by 2028 due to the need for automation and enhancing

customer experience.

Expansion of Mortgage Outsourcing

The global consumer mortgage outsourcing market is expected to grow at a compound annual growth rate (CAGR) of 10.1% between 2023 and 2030. Driven by increasing demand and the complexity of mortgage processes.

Loan Origination and Management Market Growth

Valued at approximately $1.9 billion in 2021, the loan origination and management market is anticipated to reach $3.3 billion by 2030.

Automation and Digital Transformation

It means an investment in digitalization undertaken by almost all financial institutions in a bid to make loan origination easier and faster. The automation process is designed to assist in efficiency, boost accuracy, and hasten the approval process to keep pace with the rising demands for swifter, more user-friendly services.

Integration of AI and ML

Technological advancement in AI and ML works well toward credit score checking. The system improves accuracy and the ability to detect fraud among its functionalities. It follows that lending becomes informative in both risk management and enhancing customer satisfaction.

Key Data and Statistics

The projections for the mortgage outsourcing market, loan origination and management market, and loan origination software market are as follows-

Loan Origination Outsourcing: Key data and Statistics

Mortgage Outsourcing Market

The projected growth rate will be high between 2024 and 2032 fueled by increases in consumer demand and rising pressures causing the engagement of an ever-greater number of processes.

Loan Origination and Management Market

Approximately USD 1,897.78 million in 2021. The study can reach USD 3,308.1 million by 2030.

Loan Origination Software Market

Valued at $4.8 billion in 2022, expected to reach $12.2 billion by 2032, with a CAGR of 10.2%.

Key Growth Drivers for Loan Origination Outsourcing

Some of the key growth drivers for loan origination outsourcing include-

Increased Demand for Efficiency

Primary growth factors for loan origination outsourcing involve a rising demand for the efficiency of operations, wherein lenders require more streamlined processes and cost-cutting measures.

Technological Advancements

With AI, machine learning, and automation, loan application processing is done much faster and with a high degree of accuracy.

Regulatory Compliance

Complex financial regulations worldwide are forcing lenders to team up with specialized outsourcing firms to ensure compliance standards.

Magistral’s Services for Loan Origination Outsourcing

Magistral Consulting is a premier provider of loan origination outsourcing services that will streamline processes, lower costs, and conform to regulations for banks and other financial institutions. Our expertise includes:

Loan Application Management

We encompass the entire life cycle of a loan application, from data/documentation collection through to the first level of verification, enabling faster processing times while allowing monumental administrative burden reductions.

Credit Assessment & Underwriting Support

Our experts will do extensive credit checks and research on the customers, thereby supporting the lender’s efforts by providing actionable risk assessments to inform them of better decision-making during the underwriting of loans.

Financial Due Diligence

We perform thorough financial due diligence, including balance sheet analysis and risk assessments, to facilitate informed lending decisions.

Regulatory Compliance Management

We ensure full compliance with key financial regulations such as TILA, ECOA, RESPA, KYC, AML, and GDPR to mitigate liability risk exposure for our clients.

Portfolio Monitoring & Risk Management

The continued observation of loan performance and risk indices in order to address risks before they become significant problems.

Data Management & Reporting

We do reports and analytics on loan performance to provide useful insights for better decision-making and above-average operational efficiencies no matter the time.

Automation & Process Optimization

By applying the up-to-date technology, we help our clients automate repetitive tasks for enhanced efficacy and reduced manual errors.

About Magistral Consulting

Magistral Consulting has helped multiple funds and companies in outsourcing operations activities. It has service offerings for Private Equity, Venture Capital, Family Offices, Investment Banks, Asset Managers, Hedge Funds, Financial Consultants, Real Estate, REITs, RE funds, Corporates, and Portfolio companies. Its functional expertise is around Deal origination, Deal Execution, Due Diligence, Financial Modelling, Portfolio Management, and Equity Research

For setting up an appointment with a Magistral representative visit www.magistralconsulting.com/contact

About the Author

The article is authored by the Marketing Department of Magistral Consulting. For any business inquiries, you can reach out to prabhash.choudhary@magistralconsulting.com

Can outsourcing be tailored to different loan products?

Yes, services can be customized for personal loans, mortgages, auto loans, business loans, and other financial products.

How does outsourcing improve loan processing speed?

By leveraging automation, specialized tools, and experienced personnel, outsourcing accelerates loan approvals and disbursements.

What makes Magistral Consulting suitable for loan origination outsourcing?

Magistral offers deep expertise in financial services, regulatory compliance, data security, and advanced analytical tools to optimize loan origination processes.