Successful financing forms the crux of business growth and sustainability. Critical to acquiring much-needed capital by businesses, the process of commercial lending is greatly important and plays a vital role in any organization. This article explores the complex commercial lending process, including the current trends, recognizing opportunities in different markets, and support insights.

Thank you for reading this post, don't forget to subscribe!Understanding the Commercial Lending Process

In commercial lending process, the commercial lending requires several orderly steps that would help them in understanding the condition of a business that encompasses several key components. Below process makes the organization to achieve goal efficiently and effectively.

Application for loan

For a commercial lending process, a business needs to submit a loan application. Such an application paper contains the amount of loan in desire, the purpose of the loan, and most importantly the details about the business are encoded in it, which may include financial health and operational objectives.

Collection of Documents

There are so many documents that lenders will demand to assess the sound financial position of the business, among them hence collection of documents is essential in lending process.

Financial Statements

In the process of assessing Profitability and cash flows, lenders engage in financial statement navigation involving balance sheets and income statements.

Tax Returns

Personal and business tax returns are very important measures of income and financial soundness in evaluating how lenders navigate.

Business Plan

The company should have aims, strategies, and how the loan will assist in creating growth as well as making a detailed business plan.

Credit Rating

In this process the lenders have to check his credit history and score for assessing his credit worthiness.

Credit History

The pattern of the history of past borrowing behavior would clearly outline how repayment dependable a consumer is.

Credit Score

Good credit score contributes significantly to the approval of loans and terms.

Assessment of risk

Assessment of risk includes analyzing of risks that could affect the business. Below are the various components that may affect the efficiency of a business through analyzing industry trends and economic conditions.

Industry Trends

Focusing on the market landscape will enable lenders to anticipate trends, challenges, and opportunities available.

Economic Conditions

The interest and inflation rates are the macroeconomic indicators that play a crucial role in a lending decision.

Underwriting

The underwriting stage involves checking all gathered information to establish if the loan will be viable. At this stage, financial risks are evaluated, and the terms of the loan are established, including the interest rate and repayment schedule.

Decision Making

The lender bases the final determination on the assessment of an underwriting decision. Approval means that the lender communicates all terms and may include covenants and conditions to make accurate decision which may benefit the organization.

Loan Closing

In loan closing both parties close the deal and sign the loan documents by the business

in committing itself to the terms of the loan.

Disbursement of Funds

At the time of loan’s closure, the money is disbursed and this thereafter enables the business to apply the much-needed capital.

Monitoring and Repayment

Lenders will track the business during the period of the loan to ensure that it operates within the loan agreement. The business, on its part, will repay the loans accordingly.

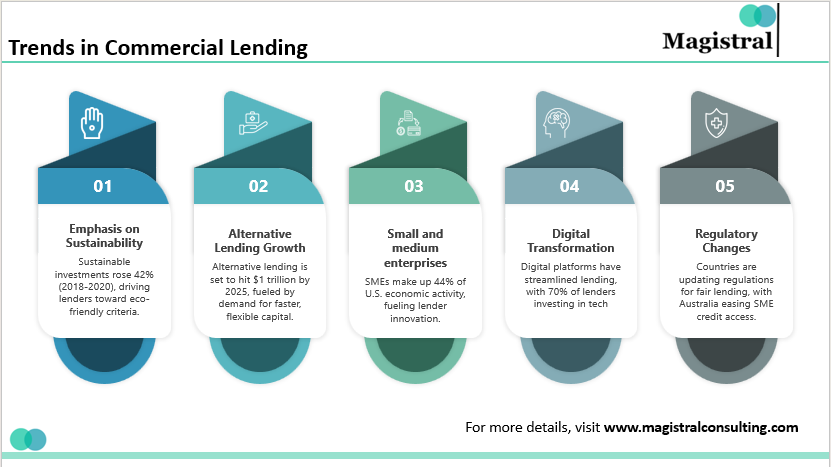

Trends in Commercial Lending

Commercial lending trends are moving towards more digital solutions, flexible loan options, and a growing emphasis on sustainability and ESG goals.

Trends in Commercial Lending

Digital Transformation

This efficiency, however, has enabled firms to streamline lending as through the development of a digital application and processing platforms with high efficiency. As reports by McKinsey published last year 2022 attest, nearly 70 percent of lenders are putting significant investments in technology.

Emphasis on what is important: small and medium enterprises.

Small and medium enterprises play a vital role in the economy of the world. An example of this is where it has been stated that the Small Business Administration of the United state has specified that in 2022, small businesses account for 44% of U.S. economic activity. Now lenders are becoming aggressive to formulate products that should cater to the needs of SMEs to ensure growth and innovation.

Alternative Lending Growth

Alternative lending platforms include online lenders and peer-to-peer lending. The World Bank is of the opinion that this market will reach $1 trillion by 2025, driven by the increasing demand for quicker access to capital and flexible terms.

Emphasis on Sustainability

This has made most lenders include sustainability criteria in their lending decisions, which is a sign that the world is slowly drifting towards more responsible lending practices. The Global Sustainable Investment Alliance reports that assets under sustainable

investments grew by 42% between 2018 and 2020.

Regulatory Changes

Countries are revising the regulatory framework to enhance the practice of fair lending and increase competition. Hence, for example, the most recent changes in regulations that have been implemented in Australia aimed at enhancing access to credit for SMEs as well as removing obstacles from the way of new lenders.

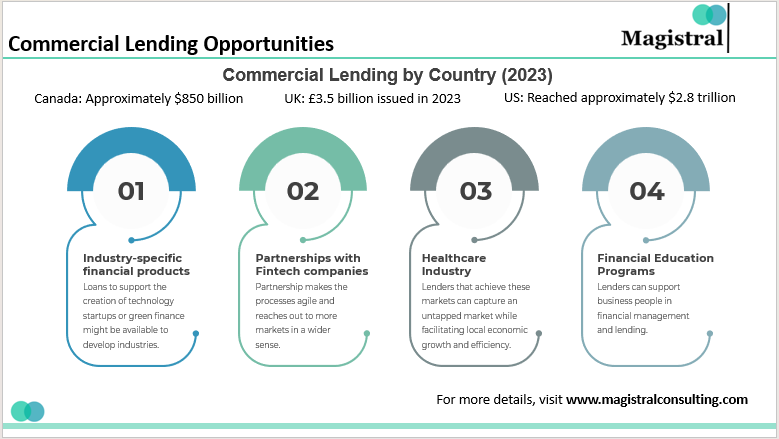

Commercial Lending Opportunities

As seen, there is various opportunities in commercial lending like industry specific financial products, partnership with fintech companies, Untapped market, financial education programs. Let’s know the points in brief:

Commercial Lending Opportunities

Industry-specific financial products

The industry-specific financial products can be developed for any one of the specific industries or business activities. Thus, loans to support the creation of technology startups or green finance might be available to develop industries in such sectors which may help to focus on industry specific products.

Partnerships with Fintech companies

Partnership will help in getting new technology, smooth working, and treating customers well. Partnership makes the processes agile and reaches out to more markets in a wider sense.

Untapped Markets

Some companies work in rural or underbanked markets where mainstream access to banking services is little. Lenders that achieve these markets can capture an untapped market while facilitating local economic growth and efficiency.

Financial Education Programs

Lenders can support businesspeople in financial management and lending. They can help potential borrowers make smart decisions through the availability of all resources and training workshops that ensure the knowledge of the borrower.

Services offered by Magistral Consulting for Commercial Lending

The operational processes of lenders need to be agile and cannot afford to go wrong in due diligence and compliance. Our services for lenders not only improve the speed of execution but the confidence with which the lending decisions are taken. Here is what we do.

Financial Projections

Estimation of future financial performance given certain assumptions.

Financial Models

Design detailed models of financial scenarios to direct decisions.

Cash Flow Models

Cash inflow and cash outflow analysis

Covenant Monitoring

Monitoring the compliance of loan agreement with financial covenants.

Credit Risk Reviews

To evaluate the creditworthiness of a borrower by analyzing the risk associated with lending money to him.

Pre-Qualification Credit Assessment

Evaluation of the financial value of a borrower prior to one’s application.

Target Screening

Target detection and evaluation of potential investment or acquisition targets.

Underwriting

Risk and terms of finance to be issued, considered for approval

Capital Structure Analysis

Determination of the company’s ratio of debt and equity financing

Credit Monitoring

Periodic review of the creditworthiness of clients or borrowers

Lending Operations Outsourcing

The provision of lending operations through external third-party suppliers.

About Magistral Consulting

Magistral Consulting has helped multiple funds and companies in outsourcing operations activities. It has service offerings for Private Equity, Venture Capital, Family Offices, Investment Banks, Asset Managers, Hedge Funds, Financial Consultants, Real Estate, REITs, RE funds, Corporates, and Portfolio companies. Its functional expertise is around Deal origination, Deal Execution, Due Diligence, Financial Modelling, Portfolio Management, and Equity Research

For setting up an appointment with a Magistral representative visit www.magistralconsulting.com/contact

About the Author

The article is authored by the Marketing Department of Magistral Consulting. For any business inquiries, you can reach out to prabhash.choudhary@magistralconsulting.com

[sp_easyaccordion id=”3201″]