Introduction

Twenty-five percent of consumers discovered errors in their credit reports, which could potentially impact their credit scores, according to Federal Trade Commission research. In today’s highly competitive business world, lenders are always searching for ways to reduce risk while promoting positive client relationships.

Credit monitoring services for lenders have emerged as a valuable tool, offering a comprehensive approach to both objectives. On the bright side, there are multiple ways to monitor businesses’ credit reports for fraud and errors. You have the choice of creating a free, do-it-yourself approach or paying for a credit monitoring service to help you. If you’re considering a paid credit monitoring service, you will need to decide if it’s worth the cost. Here is what you need to know to decide if the benefits of fee-based credit monitoring outweigh the fees.

How to Choose a Credit Monitoring Services for Lenders

Start by evaluating why your business needs a credit monitoring service. For example, if you’re already a victim of identity theft, choose a company that monitors all three of the major credit bureaus. Likewise, select a provider that offers high identity theft insurance coverage and additional features like dark web scanning.

Needs vary, but consider these general factors when choosing credit monitoring services for lenders:

- Cost. Credit monitoring services for lenders usually charge a monthly fee. However, many provide a discount for businesses that pay annual subscriptions. There are also free credit monitoring services on the market, but these offer fewer comprehensive features than paid competitors.

- The number of credit bureaus monitored. The best credit monitoring services for lenders offer triple-bureau protection. Free monitoring services and entry-level packages often include only one bureau

- Credit score model. The score reported by credit monitoring services for lenders varies by provider. While some provide users with their FICO Score, others only include the Vantage Score. FICO is the commonly used scoring model in the lending context, making it the best option for those preparing to mortgage a home or make another major purchase.

- Identity theft insurance. Many of the best credit monitoring services for lenders offer up to $1 million in identity theft insurance, while others limit coverage to $500,000 or less. Keep in mind, though, that free monitoring services often include lower coverage or none.

- Availability of dark web scanning. Most credit monitoring services for lenders also include identity protection services, including dark web scanning. This feature can help consumers protect their personal information like their individual and family members’ social security numbers.

Credit monitoring terms to know

Before you decide on your credit monitoring strategy, get to know some key terms:

- A credit monitoring service is a tool, app, or website that constantly monitors your credit report and automatically alerts you to any changes or activity that could affect your credit score.

- Free credit monitoring refers to methods or services that enable credit monitoring at no cost.

- Paid credit monitoring is a credit monitoring method or service that charges a subscription fee

- Tri-bureau credit monitoring looks at credit reports from all three credit bureaus

- Single-bureau credit monitoring looks at a single credit report from one credit bureau.

- Any alterations or questionable activities found in your credit report are sent to you via a credit monitoring alert.

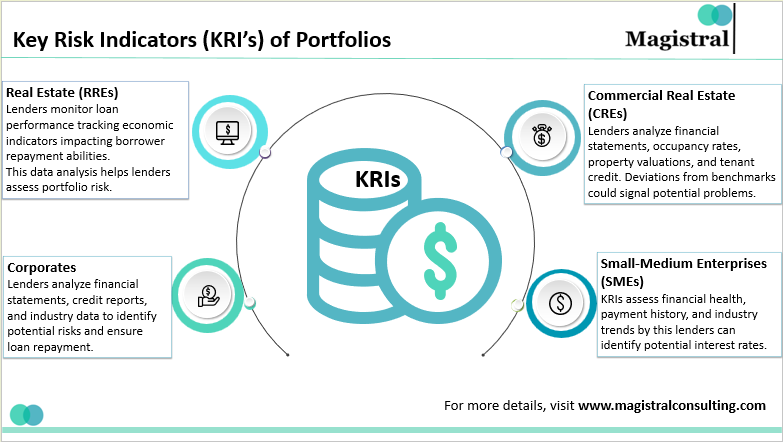

Understanding Key Risk Indicators (KRIs)

KRIs are quantitative measures that evaluate a borrower’s creditworthiness and the overall risk profile of a loan portfolio. Depending on the type of loan, different KRIs may be used for different situations by lenders.

Understanding Key Risk Indicators (KRIs)

- Corporate Loans: Total Debt to EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization), Debt Service Coverage Ratio (DSCR), and Interest Coverage Ratio (ICR) are common KRIs for business loans. These ratios evaluate a borrower’s capacity to produce enough cash flow to cover their loan payments.

- Real Estate Loans (RRE): Two important KRIs for RRE loans are the Loan-to-Value (LTV) Ratio and Debt Yield. Whereas Debt Yield shows the property’s yearly return on the loan amount, LTV compares the loan amount to the property’s worth.

- Commercial Real Estate (CRE): LTV (Loan-to-Value Ratio) and DSCR (Debt Service Credit Ratio) are major credit monitoring parameters for CRE loans. Additionally, the Loan Service to Income Ratio (LSTI) is a major indicator that evaluates a company’s capacity to generate enough rental income to cover loan payments.

- Small and Medium-Sized Enterprises (SMEs): Total Debt to EBITDA and Debt Service Capacity Ratio are major SMEs’ credit monitoring tools for lenders. These metrics evaluate an SME’s ability to manage its debt burden.

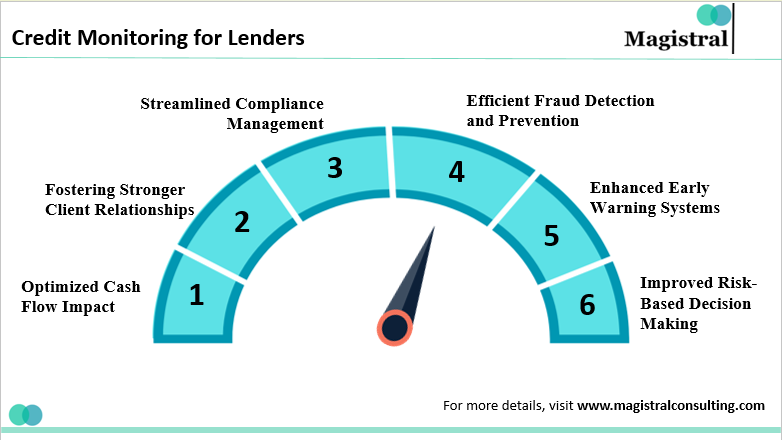

Benefits of Credit Monitoring Services for Lenders

Benefits of Credit Monitoring Services for Lenders

- Enhanced Early Warning Systems: Lenders receive real-time pop-ups from credit monitoring firms about any notable alterations to a borrower’s credit profile. This includes pop-ups on the opening of new accounts, delinquencies, queries, verdicts, and updates to public records.

- Improved Risk-Based Decision Making: Lenders can obtain risk scores from credit monitoring by using sophisticated analytics on the gathered information. Richer risk evaluations are made possible by these dynamically adjusted ratings, which adapt to variations in a borrower’s credit profile. Using real-time data instead of relying only on static credit research, gives lenders the ability to make educated decisions about loan approvals, interest rates, and credit limitations.

- Efficient Fraud Detection and Prevention: Credit monitoring services for lenders can search for situations in which a borrower’s personal information may have been stolen by integrating with dark web monitoring technologies.

- Streamlined Compliance Management: An important part of the lending business is regulatory compliance. The Fair Credit Reporting Act (FCRA) and the Gramm-Leach-Bliley Act (GLBA) are two examples of laws pertaining to credit reporting and identity theft protection that credit monitoring services can assist lenders in adhering to. Credit monitoring services may expedite compliance procedures and lower the possibility of regulatory infractions by offering a consolidated platform for tracking borrower information and creating audit trails.

- Fostering Stronger Customer Relationships: Credit monitoring services for lenders are a useful instrument for establishing goodwill among clients and constructing trust. Lenders show their dedication to safeguarding their clients’ financial security by granting access to their credit monitoring services to borrowers.

Magistral’s Services for Lenders

Lenders are highly sophisticated in an era where complexity in both new and established industries is on the rise. Financiers find it challenging to align their staffing needs with their project pipelines. Lenders’ operational procedures must be flexible and failsafe when it comes to compliance and due diligence. Magistral’s services for lenders increase the confidence in lending decisions made, in addition to the speed of execution.

Commercial Real Estate Lending

Magistral’s innovative services disrupt the traditional commercial real estate (CRE) lending market and expedite the loan application process. By doing away with manual processes like pre-qualifying borrowers and expediting property evaluations, data analytics can speed up loan approvals. The transparent, user-friendly process that offers competitive rates and real-time communication is advantageous to borrowers. Our platform creates an effective and data-driven CRE lending ecosystem, which benefits lenders and borrowers alike.

Leveraged Lending

Magistral serves borrowers looking for growth capital by providing a simplified leveraged lending procedure. They focus on alternative data sources outside of traditional financial statements and use proprietary technology to speed up credit analysis and due diligence. this process minimizes upfront costs and permits close collaboration with borrowers to customize loan structures. Magistral’s approach places a strong emphasis on effectiveness and adaptability for borrowers looking for quick and focused access to funding.

Retail Lending

Magistral evaluates the creditworthiness and risk profiles of borrowers by utilizing sophisticated data analytics. Personalized loan offers and instant pre-approvals are given to borrowers. Following that, committed loan specialists lead candidates through a more straightforward manual application and verification procedure, guaranteeing a quicker and more transparent loan approval process.

About Magistral Consulting

Magistral Consulting has helped multiple funds and companies in outsourcing operations activities. It has service offerings for Private Equity, Venture Capital, Family Offices, Investment Banks, Asset Managers, Hedge Funds, Financial Consultants, Real Estate, REITs, RE funds, Corporates, and Portfolio companies. Its functional expertise is around Deal origination, Deal Execution, Due Diligence, Financial Modelling, Portfolio Management, and Equity Research

For setting up an appointment with a Magistral representative visit www.magistralconsulting.com/contact

About the Author

The article is authored by the Marketing Department of Magistral Consulting. For any business inquiries, you can reach out to prabhash.choudhary@magistralconsulting.com

How does using Magistral for credit monitoring help you avoid scams?

Magistral's surveillance can spot abrupt or questionable shifts in a lender's credit ratings, which may raise red flags regarding possible fraud or financial hardship. In addition to standard monitoring, Magistral can provide a more comprehensive review of the issuer's credit situation, possibly revealing irregularities or hidden liabilities that manual due diligence might overlook.

How can lenders benefit from outsourcing Capital Structure Analysis using Magistral?

The skilled analysts at Magistral thoroughly examine financial data to offer a thorough evaluation of borrower risk profiles. This gives lenders more confidence to make well-informed credit decisions. By releasing capital structure analysis, lenders can concentrate on their core skills, which include relationship building and loan origination, while also freeing up valuable internal resources. Lenders can expedite loan approvals and close deals more quickly thanks to Magistral's streamlined processes, which deliver results more quickly.

In what ways can Magistral assist lenders involved in Asset-based lending?

Magistral reduces risk for lenders by thoroughly analyzing borrowers' assets to determine their actual worth. Our due diligence provides a deeper understanding of a borrower's operational efficiency and risk profile, going beyond financial statements. We customize loan agreements using our experience to help asset-based lenders minimize risk and maximize returns.