Introduction

Mortgage financing is a vital pillar in the dynamic and constantly changing world of global finance, enabling people and organizations to realize their real estate goals. However, the mortgage financing procedure is frequently fraught with complications and difficulties, taking into account a variety of elements like credit evaluations, property appraisals, legal compliance, and constantly shifting market conditions. Financial institutions’ competence is required to successfully assist borrowers through this complex maze while maintaining their own risk management.

Thank you for reading this post, don't forget to subscribe!Financial institutions, in their pursuit of excellence, aim to streamline the mortgage lending process by utilizing the specialized services provided by Magistral, a well-known outsourcing partner valued for its broad range of research and analytic skills. By offering comprehensive solutions to international businesses in a number of areas, such as investment research, procurement and supply chain intelligence, and strategy and marketing support, Magistral has established itself as a recognized industry authority.

Steps Involved in the Mortgage Lending Process

The mortgage lending process can be difficult and time-consuming. It typically involves the following steps:

Steps Involved in the Mortgage Lending Process

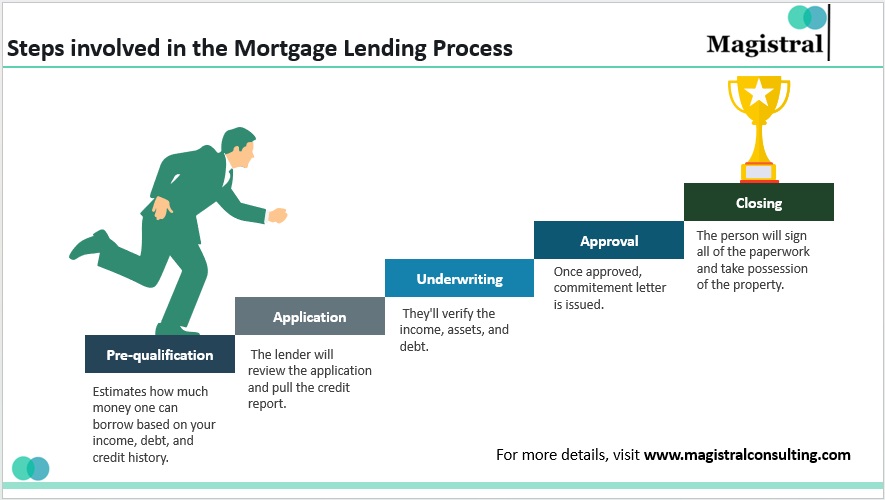

Pre-qualification

This is a process where a lender estimates how much money one can borrow based on your income, debt, and credit history.

Application

Once a person has found a home that one wants to buy, he/she needs to apply for a mortgage. The lender will review the application and pull the credit report.

Underwriting

The lender will then underwrite the loan, which means they’ll verify the income, assets, and debt. They’ll also order an appraisal of the property.

Approval

If the loan is approved, the lender will issue a commitment letter, which outlines the terms of the loan.

Closing

The final step is the closing, which is when the person will sign all of the papers and take possession of the property.

Challenges in Mortgage Lending Process

Credit Prerequisites

Credit Score Importance

Lenders take credit scores into account when determining a borrower’s creditworthiness, and higher scores frequently result in better loan terms.

Overcoming Credit Obstacles

Those with less-than-perfect credit may have a tough time getting the loan terms they want, but they can look into solutions like credit restoration or government-backed loan programmes.

Verification and Documentation

Gathering and Organizing Paperwork

The mortgage application process necessitates extensive documentation, and it can be difficult to ensure that all required information is precise and comprehensive.

Managing the Complications of Job and Income

People who are self-employed or have erratic sources of income could find it challenging to provide the required income proof.

Complex Closing Methodologies

Understanding Closing Costs

Borrowers may find it difficult to understand and budget for closing expenses, which include a variety of fees related to the loan and the transfer of ownership.

Managing Unforeseen Delays

Unexpected problems, like title challenges or financing setbacks, can cause closing delays, necessitating persistence and proactive communication from all parties.

Benefits of Streamlining the Mortgage Lending Process

Benefits of Streamlining the Mortgage Lending Process

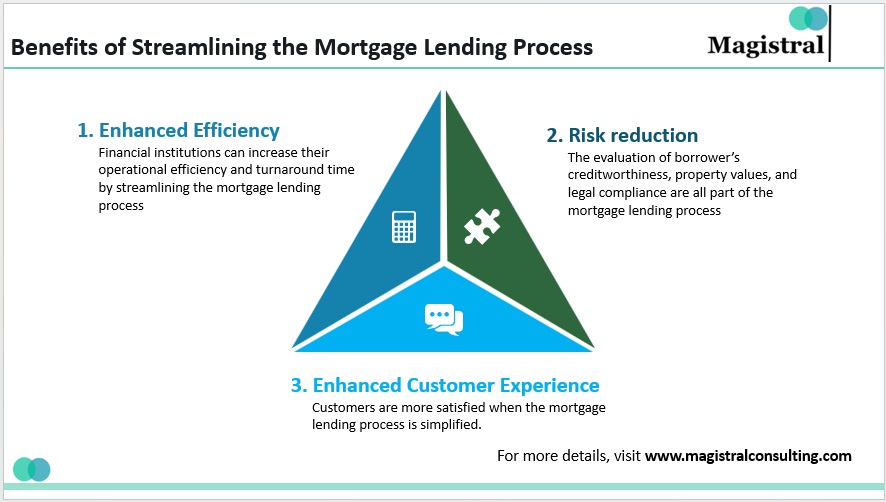

Enhanced Efficiency

Financial institutions can increase their operational efficiency and turnaround time by streamlining the mortgage lending process and cutting back on the time it takes to review loan applications. The insights and analyses offered by Magistral’s services enable lenders to make quick, well-informed judgments.

Risk Reduction

The evaluation of borrowers’ creditworthiness, property values, and legal compliance are all part of the mortgage lending process. A full risk evaluation is made possible by Magistral’s research and analytic capabilities. Thus, ensuring that lenders have a clear grasp of potential hazards and are able to make wise lending decisions.

Enhanced Customer Experience

Customers are more satisfied when the mortgage lending process is simplified. Financial institutions may improve client experiences by cooperating with Magistral to provide a smoother and more transparent application process, quicker approval time frames, and improved contact with borrowers.

Magistral’s Services on Mortgage Lending Process

With the help of Magistral’s extensive service offering, which includes investment research, supply chain intelligence, strategy and marketing support, data analytics and risk management, as well as compliance and regulatory support, both borrowers and lenders can become more efficient, make informed decisions, and successfully complete their mortgage lending goals.

Data Analytics and Risk Management

Assessing Credit Risk

Magistral’s data analytic skills can assist lenders in accurately assessing credit risk, enabling more informed lending decisions and reducing default risks.

Enhancing Loan Portfolio Management

By looking at loan portfolios, Magistral can offer insightful analysis and suggestions on how to improve loan performance, reduce risk, and increase profitability.

Support for Strategy and Marketing

Developing Targeted Marketing Campaigns

Magistral can help lenders create effective marketing strategies to connect with new borrowers, increase client acquisition, and improve overall brand positioning.

Optimizing Customer Acquisition Strategies

Using data analytics and industry insights, lenders may improve their customer acquisition tactics by finding and focusing on the most qualified borrowers with the assistance of Magistral.

Support for Compliance and Regulation

Navigating Complex Mortgage Regulations

Achieving compliance with legal and industry standards while negotiating the complicated world of mortgage laws is made possible by Magistral’s knowledge of compliance and regulatory issues.

Ensure industry standards are followed

Magistral may assist in developing and maintaining strong compliance frameworks, assisting lenders in reducing compliance risks and upholding industry best practices.

About Magistral Consulting

Magistral Consulting has helped multiple funds and companies in outsourcing operations activities. It has service offerings for Private Equity, Venture Capital, Family Offices, Investment Banks, Asset Managers, Hedge Funds, Financial Consultants, Real Estate, REITs, RE funds, Corporates, and Portfolio companies. Its functional expertise is around Deal origination, Deal Execution, Due Diligence, Financial Modelling, Portfolio Management, and Equity Research

For setting up an appointment with a Magistral representative visit www.magistralconsulting.com/contact

About the Author

The article is authored by the Marketing Department of Magistral Consulting. For any business inquiries, you can reach out to prabhash.choudhary@magistralconsulting.com

[sp_easyaccordion id=”2845″]