There were resiliency, recalibration, and geographic differentiation in the Asia-Pacific landscape of PE or private equity fund activity in 2024. While fundraising activity dropped to its lowest level since 2013, buyout investment activity showed unexpected resiliency, buoyed by mega-deals, increased public-to-private activity, and greater appetite for structured and minority investments. Meanwhile, venture capital (VC) continued its decline, investor caution favored established managers over emerging managers.

Thank you for reading this post, don't forget to subscribe!Geographically, Australia, Korea, and Japan were stand-out performers in a down market, while China and India were characterized by strategic slowdowns, largely in line with portfolio-level realignments and market corrections. Currency diversification was another trend in 2024, as local currency-denominated funds, particularly denominated in yen, attracted interest in an era of unprecedented currency uncertainty and the threat of further inflation.

>As the industry transitions to 2025, private equity firms and private equity fund face an increasingly regulated, digitized and sector-specialized environment. The global PE sector is expected to confront fundamental changes to the methods by which capital is raised, deployed and returned because of enhanced regulatory scrutiny, technology-enabled due diligence, more diversified exit strategies and more global deal making capabilities.

Current Market Performance

In Q1 2025, private equity deal activity soared, with deal volume 45% above the same quarter last year. Despite an appealing start, the emergence of rising trade tensions has created an immense degree of uncertainty, causing many investors to take a more cautious tone. As such, there may be firms that slow their investing pace temporarily in the coming months.

>That said, investors still have an appetite for risk, indicating that companies will still make quick decisions when they see attractive businesses in the market. Many are also doubling down, creating value and promoting operational improvements with current portfolio companies. Additionally, investors are looking towards resilient, strategic sectors such as Aerospace and Defence.

Current Market Performance

The re-emergence of corporate buyers has also provided an additional exit channel to stimulate exit activity, a notable change within the private equity landscape. Firms overall had strong momentum entering 2025 and a strong need to deploy a large share of the US$1.6 trillion of dry powder existing in the industry, although the aperture for deploying some of that capital is now tempered by geopolitical uncertainty.

Buyout Investments

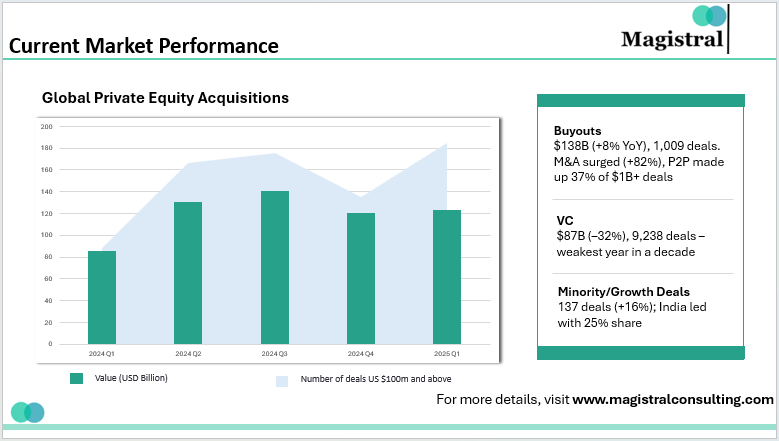

Buyout deals in the Asia-Pacific reached $138B in 2024, up 8.1% from $127B in 2023, making it the second-highest year in a decade, behind 2021. Despite a slight dip in deal count to 1,009, activity remains above pre-2021 levels, and the rate of decline in deal numbers is slowing. M&A buyouts dominated the landscape, with deal value rising 82% year-over-year. Even excluding two mega-deals (AirTrunk and Nord Anglia Education), buyout value still rose 18%. Public-to-private (P2P) deals held steady in the large-cap space, making up 37% of billion-dollar transactions, far above the 2018–2022 average of 14%.

Venture Capital Investments

VC investments continued their slump, falling to $87B across 9,238 deals—a 32% drop in value and 15% in volume from 2023. It marked the worst year in a decade by deal count and the second worst by value.

Minority and Growth Deals

There’s growing interest in structured and minority investments. These reached 137 deals in 2024, up 16% YoY. India led this segment, contributing 25% of the region’s total. Major transactions included Mubadala’s $444M pre-IPO investment in Manipal Health and TA Associates’ $396M growth funding in Vastu Housing Finance.

Geographic Insights: Key Markets and Deal Trends

Australia and New Zealand led Asia Pacific by deal value in 2024, reaching US$30.2B—over half from the US$16.1B AirTrunk transaction, the region’s largest. Without AirTrunk, the deal value was US$14.1B, slightly above 2023, ranking the region fourth. Deal count dropped 10% YoY to 168.

China ranked second with US$28.4B across 159 deals, like in 2023. However, US$18.8B came from five large portfolio management deals rather than new investments.

>Japan had the highest deal count but fell to fourth in deal value due to a lack of mega deals like Toshiba and JSR in 2023. Several large transactions are in the pipeline for 2025.

Geographic Insights: Key Markets and Deal Trends

Korea ranked third by value with US$ 18.6 B. While deal count fell to 103, activity surged in H2 2024, with US$12.9B—up 68% from the same period in 2023.

India’s buyout market slowed, with deal value down 30% to US$12.8B and deal count down 26% to 132. This is more likely a market correction to the substantial prior growth than investors losing interest.

>Funds in Asia Pacific expanded beyond their region and closed a record 82 deals (up 21% YoY) outside of Asia Pacific. The average deal size grew to US$274M from US$109M, and three of the top 10 deals from the region were outside Asia Pacific.

Private Equity Trends 2025

Private equity is still a major part of global M&A and capital markets, but in 2025, we see key changes that affect the industry that stem from changing regulations, technology, and deal strategies. Here’s a quick summary of what is likely to impact the private equity industry in 2025:

More Regulation and SEC Scrutiny

The SEC is ramping up disclosure requirements on fees, ESG, and performance measurement. New reforms on public and private equity capital markets aim to simplify transactions, reporting, and disclosures, particularly about carried interest and fund performance. These changes will affect how deals are structured, will increase compliance costs, and will probably drive firms to improve due diligence and reporting processes.

Tech-Enabled Due Diligence

PE firms and private equity fund are leveraging sophisticated data rooms and predictive analyses. It is to improve the evaluation of and engagement with deals. Artificial intelligence and big data facilitate forecasting, optimize compliance, and mitigate manual errors in filings with the SEC (which improves administrative work).

More Sector-Focused Funds

Specialty funds in healthcare, technology, and energy are gaining traction, as limited partners can offer deeper levels of industry experience. They ultimately offer greater value creation to sponsored investments. However, sector-driven private equity fund funds present regulations and compliance in a much more complex offering. e.g., compliance offerings driven by HIPAA, environmental compliance, etc. Limited partners that focus on achieving returns and want to support focused, sustainable returns prefer specialty funds.

Diverse Exit Strategies

Firms are combining realizations through IPOs, secondary buyouts, or strategic sales. Increased regulatory oversight of M&A means PE firms and private equity fund must effectively manage disclosures. There are also antitrust issues during an exit event, especially for deals in such markets or in cross-border transactions.

Cross-Border Expansion

Global deals are on the rise, but navigating different tax laws, securities regulations, and geopolitical risks remains complex. Firms must bolster compliance, especially with trade sanctions. They should work closely with local experts to ensure smooth transactions.

Digital Transformation in Portfolio Companies

PE firms are investing in AI, automation, and digital tools to boost portfolio company performance before exit in private equity fund. With growing cyber risks, strong data privacy and security frameworks are essential. Showcasing these tech upgrades in financial statements can enhance valuation and investor appeal of private equity fund.

Magistral’s Services for Private Equity Fund

Magistral Consulting has a full suite of services for private equity fund through the entire Investment Lifecycle. It also includes but is not limited to Fundraising to exit. Services for private equity fund include-

Fundraising Support

We help you develop polished Private Placement Memorandum (PPM), pitch decks and teasers. It helps to properly communicate your fund’s strategy and opportunity. We profile and outreach to investors to connect you with the right LPs. We also help you with CRM and database management to track and engage with investors.

Deal Origination & Screening

Magistral Consulting supports private equity fund by helping potential investors discover quality investments across sectors and worldwide. We manage your deal flow, from initial screening to close, and offer market and industry insights to your investment strategy.

Due Diligence and Execution of Deals

For a private equity fund, we perform detailed financial due diligence by assessing financial health and financial forecast. We also perform operational due diligence to assess the scale of target companies for the private equity fund. In terms of valuation support, we perform DCF and comparable company/cash flow valuation. We also write investment memorandums to assist in clearly presenting deals to investors.

Portfolio Management and Exit Planning

For private equity fund, we provide portfolio ESG monitoring and financial reporting for portfolio companies. It involves compliance and reporting on performance. We provide strategic value improvement to portfolios, and we assist in exit planning and execution. This also includes IPOs and secondary buyouts, to maximize total returns at exit.

About Magistral Consulting

Magistral Consulting has helped multiple funds and companies in outsourcing operations activities. It has service offerings for Private Equity, Venture Capital, Family Offices, Investment Banks, Asset Managers, Hedge Funds, Financial Consultants, Real Estate, REITs, RE funds, Corporates, and Portfolio companies. Its functional expertise is around Deal origination, Deal Execution, Due Diligence, Financial Modelling, Portfolio Management, and Equity Research

For setting up an appointment with a Magistral representative visit www.magistralconsulting.com/contact

About the Author

The article is authored by the Marketing Department of Magistral Consulting. For any business inquiries, you can reach out to prabhash.choudhary@magistralconsulting.com

[sp_easyaccordion id=”3802″]