Introduction

Private equity refers to investments that are made directly into a business by some investors and private equity organizations. Institutional investors typically make private equity investments in venture capital funding or leveraged buyouts. Investors use private equity for various goals, including technology upgrades, business expansion, acquisitions, or even the reviving failed organizations.

Thank you for reading this post, don't forget to subscribe!Private equity investors often have a 5-7-year investment horizon. And they are expected to leave after making a significant return on their investment. Private equity investors might use various exit strategies to get their money back. Private equity (PE) has been the expansion engine for a while. The primary goals of this industry are evolution and productivity. Private equity refers to capital that is not traded on a public market and is invested in a long-established industry that is not functioning well or is about to fail. Venture Capital, Growth Capital, Leveraged Buyout, Mezzanine Debt, and Distressed Debt are the five main types of PE. A venture capitalist, often known as a “venture capitalist,” comes to their aid by offering risk-bearing funds. Institutional and individual investors contribute funds to private equity, which can be used to fund innovative technology, boost working capital, or consolidate a balance sheet.

Standard Modes of Private Equity’s Exit Strategy From Portfolio Companies

Exits are of crucial importance to Private Equity investors, and they consider a variety of different exit strategies to realize their return on investment. Some of the most common Private Equity exit strategies include:

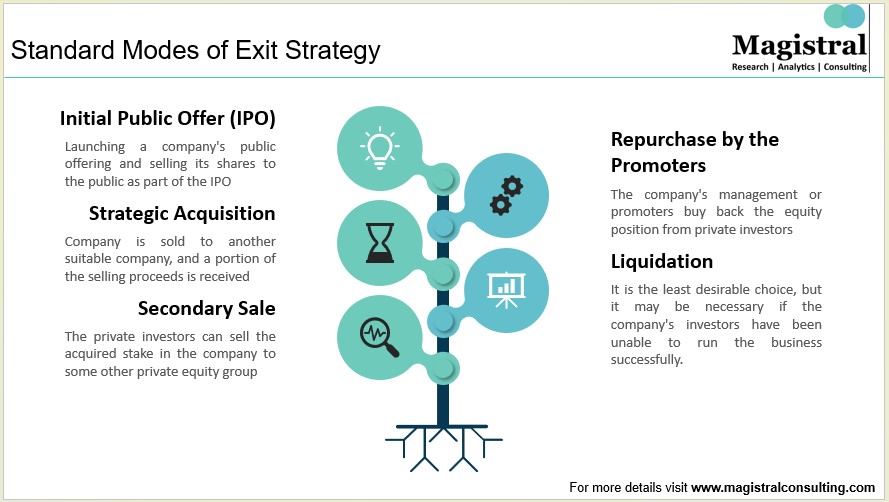

Standard Modes of Exit Strategy

Initial Public Offer (IPO)

One frequent method is to launch a company’s public offering and sell its shares to the public as part of the IPO. Depending on the situation, investors might sell shares at once. Investors can also sell assigned shares once the company is listed and trading starts on the exchange. Due to high costs, only large corporations typically undertake stock market flotation which must be financially sustainable.

Strategic Acquisition

A strategic buy or trade sale is another choice, in which the business is sold to a different suitable company and a portion of the sale earnings is received. One of the most typical methods for private equity funds to exit is this one. The buyer will typically profit strategically from purchasing this business because their strengths may compliment one another. As a result, the buyer frequently pays more to purchase such a business.

Secondary Sale

The private investors can sell the acquired stake in the company to some other private equity group in a secondary sale. The secondary sale might happen for a variety of reasons. For example, the business may demand additional funds above the current equity fund’s capability. Alternatively, the company may have reached a point where the earlier private equity investors wanted it, and additional equity investors wanted to take over.

Repurchase by the Promoters

It is another effective exit plan in which the company’s management or promoters buy back the equity position from private investors. For both investors and management, this is an appealing exit option.

Liquidation

It is the least desirable choice, but it may be necessary if the company’s promoters and investors have been unable to run the business successfully.

Key Considerations and Trends in Private Equity’s Exit Strategy From Portfolio Companies

Key Considerations and Trends in Exit Strategy

Preparing the Portfolio Company for Sale

Private Equity investors, being financial investors with an investment philosophy of creating returns on their investments. PE investors closely monitor company performance and make strategic decisions that impact valuation, especially near exit. Furthermore, as part of a portfolio company’s ‘clean-up’ prior to an impending sale. Another emerging trend is to refinance or repay the company’s existing debt to be able to, among other things:

-Displaying a solid balance sheet to potential incoming buyers

-If any, obtaining a release of encumbrances over shares of other shareholders that may be relevant for a bulk sale.

Partial Exit

Retaining a majority interest or control rights in a publicly traded firm after a partial exit may expose the Private Equity investor to be classified as a promoter or “co-promoter.” Partially exiting from a private firm carries risks. Like risk of the Private Equity investor losing control and piggybacking on the founders’ or private equity’s exit strategy.

Use of Insurance Product

Most Private Equity investments are made through funds with a short life expectancy and internal constraints on taking general indemnity obligations. As a result, using an insurance product to supplement, and in some circumstances completely replace, the indemnification structure that sellers may provide in such transactions is becoming increasingly prevalent.

Severance Payouts or Compensation Arrangements

Without board and non-interested public shareholders’ approval, a Private Equity investor cannot enter compensation or profit-sharing arrangements to company insiders. Such arrangements, including severance payouts, cannot share exit returns beyond a hurdle rate without proper approvals.

Guaranteed Returns

Debate continues on whether a foreign investor can exit at a pre-determined valuation while guaranteeing returns. Indian courts now uphold indemnity and damages claims, even if they conflict with exchange control rules on guaranteed returns.

Tax Considerations

There may be different tax implications depending on the cost of buying shares and the difference between the purchase value and the final sale price. To minimize further tax implications, investors should ensure they do not treat indemnification payments as income but instead adjusted as capital gains. They must also implement exit structures that minimize tax exposure and prevent violation of India’s “general anti-avoidance regulations.” In transactions involving selling shares by a non-resident private equity investor to another non-resident private equity investment, indemnities for potential indirect transfer taxes become an essential part of the share purchase agreements.

Enforceability of IPO provisions

Since directors sign the IPO offer documents, fiduciary duties may block IPO terms set by PE investors if not shareholder friendly. Also, the company must meet IPO eligibility norms like profitability, net worth and a minimum net tangible assets.

Locked-box vs Completion Accounts

There are two methods for making post-completion adjustments: completion accounts or a locked-box approach. A locked-box method is efficient since it ensures pricing certainty and saves management time and effort to prepare completion accounts. However, under a locked-box system, the parties may fail to adequately balance the impact of intermediate activities by relying solely on post-signing interest paid with the purchase price instead of reflecting them in completion accounts.

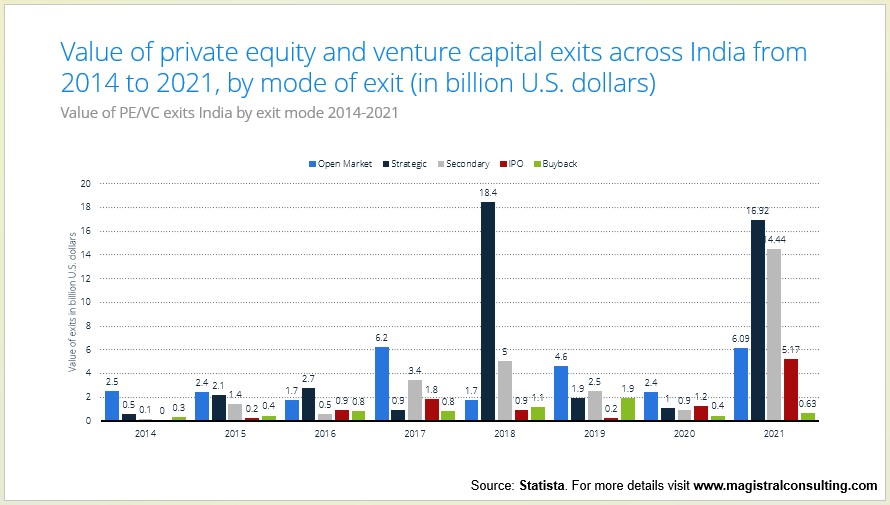

Number of private equity and venture capital exits across India

Value of Private Equity and Venture Capital Exits

Magistral’s services on Private Equity’s Exit Strategy From Portfolio Companies

Magistral’s successful exit strategy specifies existing owners’ procedures to separate themselves from the company. The extended off-shore team also ensures retention of expertise across firms for similar projects. And that numerous projects in several companies can run simultaneously, prioritized according to board meeting schedules. Unanticipated events may necessitate the implementation of a corporate exit strategy.

About Magistral consulting

Magistral Consulting has helped multiple funds and companies in outsourcing operations activities. It has service offerings for Private Equity, Venture Capital, Family Offices, Investment Banks, Asset Managers, Hedge Funds, Financial Consultants, Real Estate, REITs, RE funds, Corporates and Portfolio companies. Its functional expertise is in Deal origination, Deal Execution, Due Diligence, Financial Modeling, Portfolio Management and Equity Research.

For setting up an appointment with a Magistral representative visit www.magistralconsulting.com/contact

About the Author

The article is Authored by Marketing Department of Magistral Consulting. For any business inquiries, you could reach out to prabhash.choudhary@magistralconsulting.com