In 2025, Hedge Funds have transitioned from niche alternatives to key strategic anchors in global portfolios. With total industry AUM reaching $5.1 trillion by mid-2025, the sector is benefiting from renewed appetite among institutional and wealthy clients seeking resilience during inflation, interest rate divergence, and market volatility.

For financial services professionals, the discussion about hedge funds is no longer descriptive; it is interpretive. The central challenges are how to allocate capital across divergent regions and strategies, how to engage clients with new structures, and how to position hedge funds within broader portfolio narratives.

The Hedge Fund Industry Landscape in 2025

As Hedge funds continue to expand across regions and strategies, the growth remains uneven. North America dominates, Europe resurges, and Asia presents sharply divergent outcomes in contrast to the other regions.

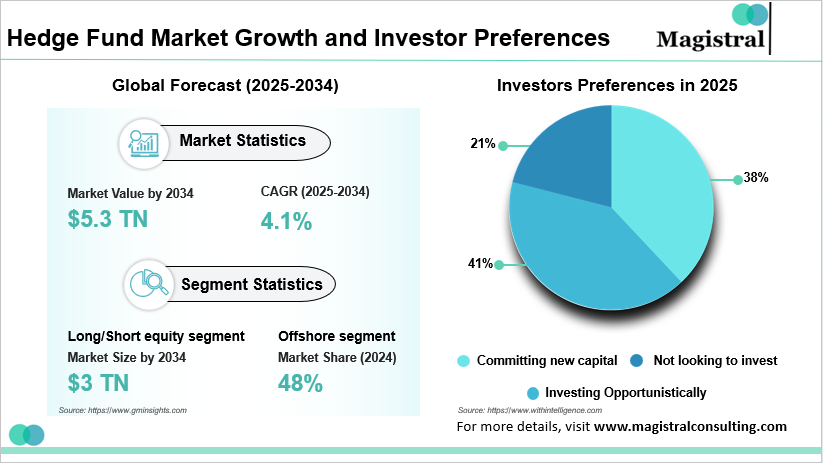

Hedge Fund Market Growth and Investor Preferences

Global AUM and Flow Trends

Hedge funds attracted $142 billion in net inflows during H1 2025, reversing the muted flows of 2023. North America accounts for the lion’s share, with $3 trillion AUM—nearly 60% of the industry. Europe contributes $1.1 trillion, buoyed by renewed M&A cycles, while the Asia-Pacific region holds $700 billion, reflecting strong inflows from India but consistent outflows from China. Middle Eastern sovereign wealth funds have become more active allocators, adding billions in niche strategies aligned with energy and infrastructure.

Strategy Performance and Investor Preferences

By June 2025, macro hedge funds surged ahead with +11.2% YTD returns, capitalizing on central bank divergence and commodity spreads. Event-driven funds followed at +8.7%, boosted by an uptick in global deal-making. Equity long/short strategies lagged with +4.3%, as AI-driven equity market dispersion challenged stock pickers. Perhaps most notably, quantitative and AI-driven funds represented over 35% of new launches, reflecting the structural integration of advanced technology into hedge fund DNA.

Interpretation for Financial Professionals

The landscape underlines a clear fact: capital is flowing toward strategies designed for dislocation, volatility, and diversification. For private banks, institutions, and consultants, hedge funds are not tactical positions but core elements of portfolio architecture.

Emergence of Multi-Strategy Platforms

Large multi-strategy managers continue to consolidate industry capital. Mega-platforms like Citadel and Millennium collectively manage more than $400 billion in AUM, offering diversification within single-manager structures. This scale attracts institutional flows but raises systemic concentration risks that regulators and allocators are closely monitoring.

Hedge Funds as Strategic Tools in a Volatile Macro Environment

Hedge funds in 2025 function as volatility harvesters, offering portfolio stability amid dislocated monetary regimes and heightened geopolitical risk. They are no longer positioned as short-term speculative plays but as systematic allocation tools designed to extract value from dispersion across markets and to act as insurance when traditional assets correlate during drawdowns.

The sector’s growing strategic importance rests on its ability to provide uncorrelated returns in environments where both equities and bonds face simultaneous headwinds, reshaping their role in portfolio construction for institutions and private wealth alike.

Policy Divergence and Volatility Harvesting

The U.S. Federal Reserve maintains rates in the 4.5–4.75% band, the ECB grapples with Eurozone inflation above 5%, and Japan’s dramatic exit from yield curve control has injected cross-market volatility. Macro funds thrive in this regime, exploiting interest rate differentials, currency opportunities, and commodity spreads. They increasingly act as risk mitigators rather than pure alpha generators, stabilizing portfolios in turbulent cycles.

Institutional Shifts in Allocation Structures

Institutions, which contribute two-thirds of global hedge fund AUM, are demanding more alignment. Fee compression continues, with 68% of allocators seeking arrangements below “2 and 20,” often tied to hurdles or performance breakpoints. Additionally, institutional capital strongly favors quarterly or semi-annual redemption schedules, rejecting extended lock-up terms. The rise of co-investment structures, now attached to nearly one in five allocations, reflects the desire for select deal exposure at reduced fees.

Liquidity as a Central Narrative

Post-pandemic lessons have sharpened allocator focus on liquidity. Hedge funds once tolerated with two- or three-year lockups now face pressure to provide partial redemption windows. For banks and advisors, structuring hedge fund offerings around liquidity-compatible SMAs or feeder funds remains a differentiating client proposition.

Hedge Funds as Portfolio Insurance

Advisors increasingly present hedge funds as defensive allocations, serving as hedges against inflation, stagflation, and dislocated bond markets. For high-net-worth clients, this framing resonates far more than speculative narratives—it positions hedge funds as tools of preservation, not only return.

Customization and SMA Access

Beyond pooled strategies, separately managed accounts (SMAs) are soaring in demand. UHNW clients and family offices prioritize transparency, direct exposure, and tailored risk mandates. Hedge fund SMAs provide this customization, while also allowing banks and distributors to maintain granular oversight of exposures.

Implications for Financial Services Institutions

For financial services platforms—private banks, wealth managers, consulting firms, and hedge funds are no longer “products” but strategic conversations. Differentiation comes from integrating hedge fund narratives into holistic client advisory: how they hedge policy dislocation, how liquidity is structured, and which strategies align with institutional capital momentum.

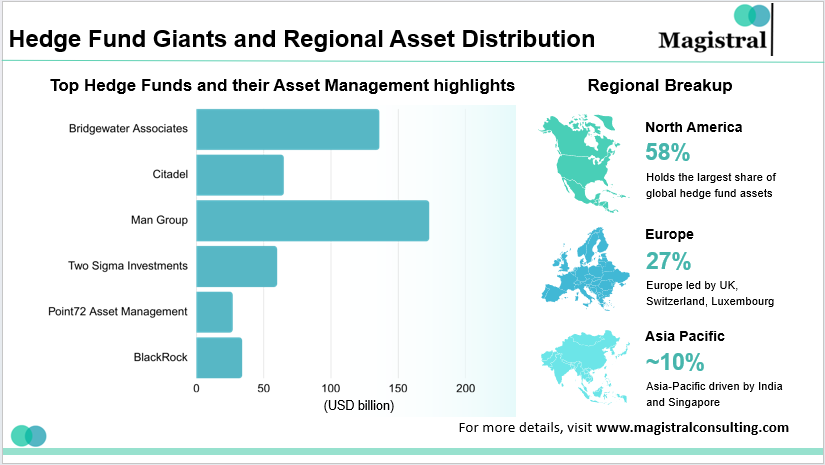

Regional Dynamics and Capital Flows in Hedge Funds

Regional divergence is shaping not just fund flows but the strategic priorities of global financial platforms, demanding region-specific solutions.

Hedge Fund Giants and Regional Asset Distribution

North America: The Mega-Platform Era

U.S.-based multi-strategy giants such as Citadel and Millennium now manage over $400B combined, absorbing disproportionate capital flows. Their scale makes them a magnet for institutional allocators seeking resilience, though concentration risk is rising.

Europe: Event-Driven Resurgence

Europe’s resurgence stems from M&A-driven event strategies, with deal volumes up 15% in 2025. London and Paris-based managers thrive, but increasing ESG disclosure rules from ESMA mean European hedge funds must align sustainability narratives with performance mandates.

Asia-Pacific: Divergent Narratives

Asia presents a split: China is losing allocator confidence, with $22B in redemptions, while India is emerging as a hedge fund growth hub with $18B new inflows on strong GDP growth (6.5%). Singapore is strengthening its role as the APAC hedge fund hub, with MAS registrations growing 20% YoY.

Middle East: Sovereign Wealth Influence

Sovereign wealth funds from the GCC, managing over $4T in assets, are raising allocations in commodity and special situation strategies. For global managers, building SWF partnerships has become central to growth.

Hedge funds in 2025 occupy a firm place as strategic anchors in capital allocation. They are not simply seeking alpha but providing portfolio stability, downside protection, and access to differentiated strategies unavailable in traditional markets.

For financial services leaders, the challenge and opportunity lies in translation: making hedge fund flows, structures, and risks accessible to clients in actionable terms. Those platforms that can balance regional nuance, integrate liquidity-compatible structures, and articulate the role of technology will strengthen their positioning as trusted advisors.

In a volatile macro world, hedge funds have transcended the “alternative” label—they are now core building blocks of institutional and wealth portfolios.

Services Provided by Magistral Consulting for Hedge Funds

Magistral Consulting offers comprehensive services tailored for the funds, covering the entire investment lifecycle. The offerings include fundamental and technical research, DCF modelling, company profiling, and sector reports to support informed decision-making. We also assist in strategy development, risk management, and performance analysis. Magistral also provides operational support through back-office outsourcing, fund administration, and investor relations management. For emerging and established funds, we offer services like due diligence, fund selection analytics, and capital introduction by preparing CIMs/PPMs and connecting with potential investors. These end-to-end solutions help enhance efficiency, ensure compliance, and optimize returns in a competitive investment landscape.

About Magistral Consulting

Magistral Consulting has helped multiple funds and companies in outsourcing operations activities. It has service offerings for Private Equity, Venture Capital, Family Offices, Investment Banks, Asset Managers, Hedge Funds, Financial Consultants, Real Estate, REITs, RE funds, Corporates, and Portfolio companies. Its functional expertise is around Deal origination, Deal Execution, Due Diligence, Financial Modelling, Portfolio Management, and Equity Research

For setting up an appointment with a Magistral representative visit www.magistralconsulting.com/contact

About the Author

Prabhash Choudhary is the CEO of Magistral Consulting. He is a Stanford Seed alumnus and mechanical engineer with 20 + years’ leadership at Fortune 500 firms- Accenture Strategy, Deloitte, News Corp, and S&P Global. At Magistral Consulting, he directs global operations and has delivered over $3.5 billion in client impact across finance, research, analytics, and outsourcing. His expertise spans management consulting, investment and strategic research, and operational excellence for 1,200 + clients worldwide

FAQs

What is the current global market size of hedge funds in 2025?

How are hedge funds adjusting to the evolving macroeconomic environment?

What role does technology play in modern hedge fund strategies?

How are fee structures changing in hedge funds?

What services does Magistral Consulting provide for hedge funds?