In private markets, raising capital is no longer a game of sending the same story to a long list of names and hoping a few meetings appear. Allocators have become more selective, fundraising cycles have stretched, and managers face tougher scrutiny on fees, reporting depth, and strategic differentiation. That is exactly why Investor Profiling has moved from a useful research exercise to a core commercial capability. When done well, it helps firms identify who is most likely to invest, what those investors care about, and how the message should be framed for each audience. The result is not just more conversations. It is better conversations, shorter learning cycles, and a far more disciplined route to capital.

Why Investor Profiling Matters in a Crowded Capital Market

Investor profiling is important as it recognizes that the capital pool is increasing, yet the route to it is becoming more crowded and more challenging. No longer does a larger capital pool automatically imply that fundraising will get easier.

Why Investor Profiling Matters in a Crowded Capital Market

Bigger markets do not automatically mean easier fundraising

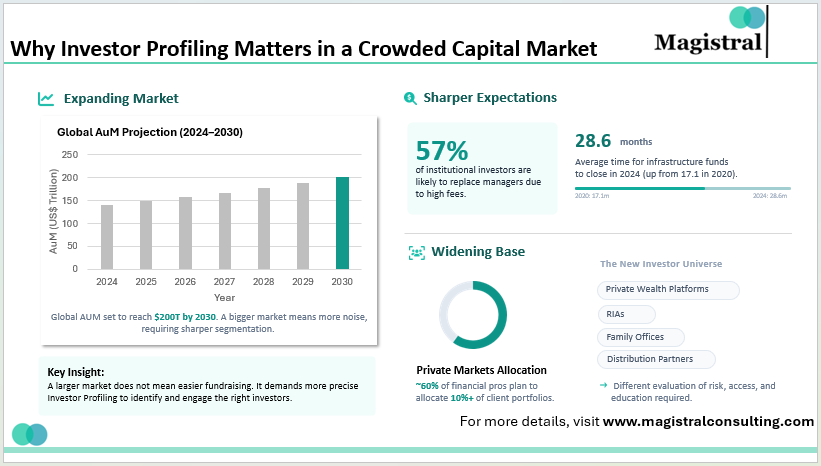

PwC forecasts that global assets under management are expected to increase from US$139 trillion in 2024 to US$200 trillion in 2030. Meanwhile, private markets revenues are expected to surpass US$432 billion, with more than half of that revenue coming from private markets by the end of the decade. That is a huge capital pool to access, yet it also represents a larger number of managers, a wider variety of products, and a more competitive environment. In this environment, it is no longer about building the biggest possible list of investors to approach; it is about having a sharper profile of investors. Firms that are currently engaged in capital raising need to have a sharper profile of investors long before they send out their first email.

Investors are demanding more value for every basis point

It’s increasingly difficult to ignore fee sensitivity. In fact, PwC found that 57% of institutional investors are likely or very likely to switch managers based on high fees. That’s a game-changer. The pitch no longer just hinges on a manager’s reputation, brand, or relationships. It’s no longer sufficient for a pitch to be well-received unless there’s a strong connection to a prospect’s mandate, liquidity, return, portfolio gaps, and reporting. Investor profiling is no longer demographic-based; it’s investable-based.

Private wealth is widening the opportunity set

The universe of investors is expanding, too. Hamilton Lane found that almost 60% of financial professionals planned to invest at least 10% of their clients’ portfolios in private markets in 2025, with 30% planning allocations of at least 20%. Why does this matter? The universe of investor profiling has changed. RIAs, private wealth platforms, family offices, and distribution partners are now part of the universe alongside pensions and endowments. Each segment has its own approach to risk, access, education, and communication. Therefore, the approach to communicating with investors must change.

The cost of getting it wrong is usually hidden

A poor target list does not often crash and burn in an explosive moment of truth. Rather, it stagnates over months because of low response rates, sluggish feedback, and a series of messaging resets, not to mention internal confusion about where the real demand is. Sometimes, a team might think it has a storytelling issue when it really has a matching issue. And this is important. Because if the wrong allocators are in the funnel, no amount of great presentation or an excellent track record will help.

Even a sector-specific fundraiser, such as infrastructure funds closed in 2024, highlights how deliberate the market is becoming. Infrastructure funds closed in 2024 took an average of 28.6 months on the road, up from 17.1 months in 2020. Although this is sector-specific, it is telling nonetheless. Managers need better qualifications, better prioritization, and better timing if they want the fundraising process to be purposeful.

Building an Investor Profiling Framework That Actually Works

Investor profiling should be viewed as a dynamic investment process rather than a one-time data collection effort. It begins with assessing objective criteria like strategy preferences and ticket sizes to focus on a smaller, higher-quality pool of potential investors. Incorporating behavioral insights, such as past commitments and engagement patterns, helps distinguish active investors from passive ones. A well-defined group of investors often yields better outcomes than a larger, less understood one. While technology can aid in data analysis, it cannot replace the need for interpreting investor alignment and intent. Continuous feedback should be utilized to refine the investor universe and narrative, creating a more adaptive fundraising model.

The real edge comes from the context, not the size. A smaller but well-understood universe of investors may often be more beneficial in terms of outcomes compared to a large but undefined universe of investors. Although technology and artificial intelligence can speed up data analysis and pattern detection, they are still not a replacement for interpreting alignment and intent. Most organizations are using technology in a very basic sense, which again brings us back to interpreting.

It is also very important to note that the investor profiling should be a dynamic system. Each touchpoint, whether it be feedback on ticket size, strategy fit, or messaging, should be used to continually enhance both the universe of investors and the narrative around investors. This will, in effect, build a much more adaptive and intelligent model of fundraising.

Managers with large ticket capacity should not receive the same approach as a family office exploring niche co-investment opportunities. At this stage, the goal is to reduce noise. A smaller list with high-probability names is usually worth more than a massive database with weak alignment.

Investor Profiling Across Different Investor Segments

Investor Profiling is most valuable when firms recognize that capital is not necessarily homogeneous in behavior. Different investor classes have different investment narratives, different risk profiles, and different investment timeframes.

Investor Profiling Across Different Investor Segments

Institutional allocators want precision and process

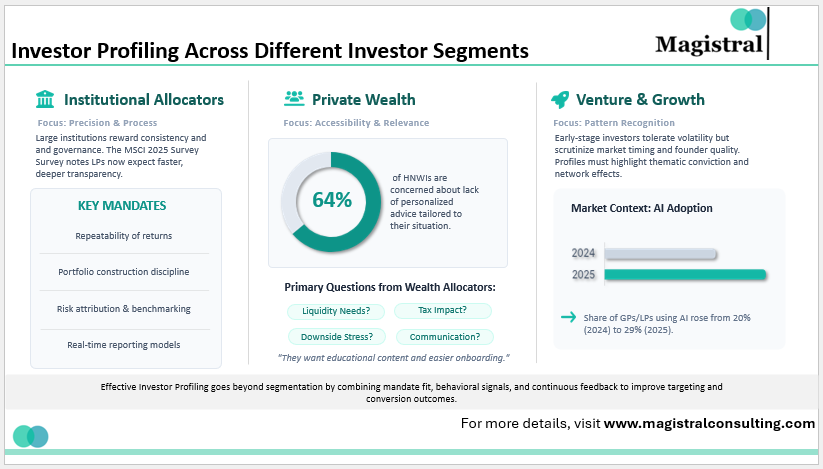

For example, the MSCI 2025 General Partner Survey found that LPs are allocating more capital, but also expect faster and deeper transparency, with increasing demands for benchmarking, risk attribution, and real-time reporting. For example, for a manager looking to reach pension or sovereign wealth institutions, it is not just about demonstrating a track record; it is about demonstrating repeatability, portfolio management discipline, and a reporting structure that can withstand scrutiny

Family offices and wealth channels want accessibility and relevance

For instance, Capgemini found that more than 64% of HNWIs expressed concern about a lack of personalized advice tailored to their financial situation.

It is not just about making their messaging more friendly or approachable; it is about creating context for their investment strategy.

It is about creating context for their investment strategy and explaining to them how this investment strategy can help them meet their liquidity needs, tax concerns, portfolio concentration, and long-term family goals.

What these investors often ask first

Some private wealth allocators tend to start with basic yet insightful questions. How much capital is likely to be drawn down, and when? What does the downside look like in a stressful scenario? How concentrated is this manager’s portfolio? How regular will updates be? And are those updates likely to be understandable to non-specialist stakeholders? A good target profile should answer these questions in advance of the first meeting, which makes for a more relevant conversation than a rehearsed one.

Venture and growth investors respond to pattern recognition

For venture and growth investors, their assessment of opportunities is likely to be different from that of those in other asset classes. A manager who is familiar with venture capital culture is likely to have to demonstrate their preference for stage, geography, sector, cash reserves, and even network effects. A name that sounds good on paper is not necessarily good in practice if this investor prefers direct deals, dislikes crowded spaces, or is overinvested in a similar space to begin with.

Sector context can reshape the target map

Managers often overlook the reality that investors’ interests will be shaped by what is going on in the market. 2025 will see an expansion of alternative strategies and the integration of AI in sales and distribution for companies. It’s reported that in 2025, 29% of GPs and LPs using AI in their processes increased from 20% in 2024. This further indicates how strategies are becoming more nuanced, which will impact how investors who are comfortable with innovation, those who prefer traditional categories, and those who need further education will be considered.

How Magistral Strengthens Investor Profiling for Fundraisers

Investor profiling is most effective when research, structured data, and execution are combined, with operational support aiding lean teams in achieving institutional-quality coverage. Magistral enhances this process by creating a targeted investor universe through mandate mapping, strategy alignment, ticket sizing, and prioritization, enabling firms to focus on high-potential prospects. Segmentation of investor lists facilitates effective outreach strategies, while ongoing support in meeting preparation, tracking, and feedback analysis fosters continuous improvement. This comprehensive approach strengthens the connection between strategy, message, and execution, ultimately leading to better investor relationships.

About Magistral Consulting

Magistral Consulting has helped multiple funds and companies in outsourcing operations activities. It has service offerings for Private Equity, Venture Capital, Family Offices, Investment Banks, Asset Managers, Hedge Funds, Financial Consultants, Real Estate, REITs, RE funds, Corporates, and Portfolio companies. Its functional expertise is around Deal origination, Deal Execution, Due Diligence, Financial Modelling, Portfolio Management, and Equity Research

For setting up an appointment with a Magistral representative visit www.magistralconsulting.com/contact

About the Author

Tanya is an investment-research specialist with 6 + years advising venture-capital, private-equity and lending clients worldwide. A Stanford Seed alumnus with an MBA and an Economics (Hons) degree, she heads project teams at Magistral Consulting, delivering financial modelling, due-diligence and deal support on 3,000 + mandates. Her blend of rigorous analytics, sharp project management and clear client communication turns complex data into actionable investment insight.