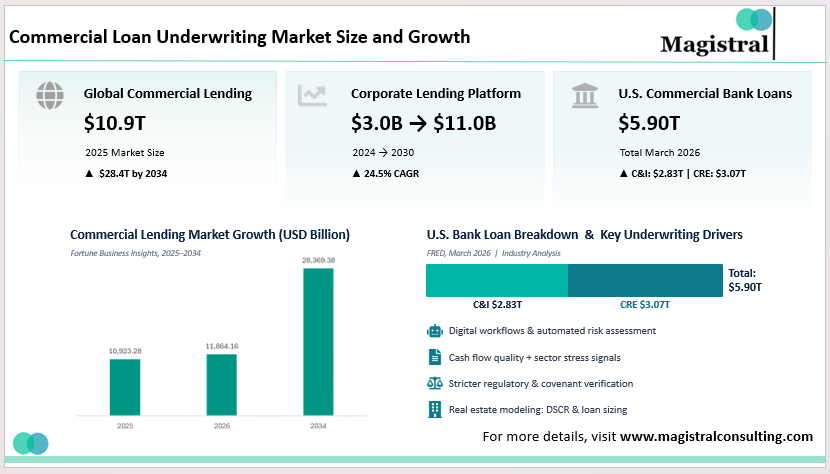

Commercial loan underwriting has evolved into a more data-intensive and regulated process, requiring greater strategic planning. Lenders now assess deals using a combination of borrower financials, asset values, sector signals, and cash flow quality, supported by faster digital workflows. This shift is driving market growth, with the global commercial lending market projected to expand from $10.9 trillion in 2025 to $28.4 trillion by 2034, alongside advancements in underwriting technology and risk assessment.

Thank you for reading this post, don't forget to subscribe!Commercial Loan Underwriting Market Size and Growth

The process of Commercial Loan Underwriting operates within an extensive lending network that continues to expand even when certain areas experience restricted credit conditions. Fortune Business Insights estimates the global commercial lending market at $10,923.28 billion in 2025 and projects $28,369.38 billion by 2034, which indicates substantial market growth during the next few decades. The corporate lending platform market will reach a value of $3.0 billion in 2024, according to MarketsandMarkets, and grow to $11.0 billion by 2030 with a compound annual growth rate of 24.5% because underwriting processes increasingly adopt digital systems and automated workflows.

Commercial Loan Underwriting Market Size and Growth

Why this growth matters for lenders

Underwriters who need to evaluate increased loan volumes must maintain their credit assessment standards while managing their workload. The lenders combine traditional review methods with analytical tools, workflow solutions, and expert assistance. Underwriting now operates through a system that combines modeling processes, documentation assessment, covenant verification, and sector analysis. The interconnected systems of real estate financial modeling become necessary in property secured transactions because even small changes in assumptions produce major impacts on both debt service coverage and loan sizing calculations.

Recent signals from the U.S. credit market

American businesses maintain their commercial credit balances at elevated levels according to the latest data. FRED reports that Commercial and Industrial Loans at all commercial banks reached about $2.828 trillion in March 2026, while Commercial Real Estate Loans at all commercial banks stood at about $3.073 trillion in the same month. The data shows that banks use Commercial Loan Underwriting as their main function because even small changes in approval criteria result in significant impacts on their credit portfolios.

Commercial Loan Underwriting Trends in Risk, Demand, and Approval Standards

The current credit standards show a dual development because some borrower segments demonstrate increasing demand while other segments maintain their existing credit standards. The Federal Reserve’s January 2026 Senior Loan Officer Opinion Survey said banks reported generally unchanged standards and stronger demand for commercial real estate loans, while expecting demand to strengthen across 2026.

Credit standards are still cautious

Credit standards maintain their cautious approach, which prevents lenders from extending credit. The FRED series shows banks expanding their lending standards to CRE construction loans, which demonstrates the industry shift from previous practices. The measure showed a decrease from 11.1 in Q2 2025 to 1.8 in Q1 2026, which shows declining pressure on underwriting standards. The risk signals continue to function while demand shows signs of improvement.

Demand is improving with risk signals intact

The same survey found stronger demand for CRE loans while asset quality remained under observation. The FDIC data shows that non-owner-occupied CRE delinquency rates reached 2.02% in 2024, which remains higher than the historical average. The structured underwriting practices that use due diligence and valuation frameworks demonstrate their critical value to the process.

Commercial Loan Underwriting and Technology Adoption

The process of Commercial Loan Underwriting has started to evolve into a function that requires technological solutions. Markets and markets projects lending platforms to grow from $3.0 billion in 2024 to $11.0 billion by 2030. The increase in this development occurs because businesses now use artificial intelligence along with automation and data analytics to improve their underwriting operations.

Practical impact of automation

The underwriter teams use technology to enhance their ability to process documents, track covenants, and assess risks at an early stage. McKinsey suggests that AI-enabled underwriting can reduce decision time significantly while improving consistency.

The solution maintains compatibility with present financial transformation efforts because Finance ecosystem connections enable better borrower profile development and monitoring activities.

Balance between automation and judgment

Both automation and human judgment must reach a state of equal equilibrium. Underwriters who possess experience make the final decision for lenders despite the system’s automated processes. Automated systems cannot handle the complete evaluation of borrower strategy, industry outlook, and potential negative outcomes, which are needed for complex deals.

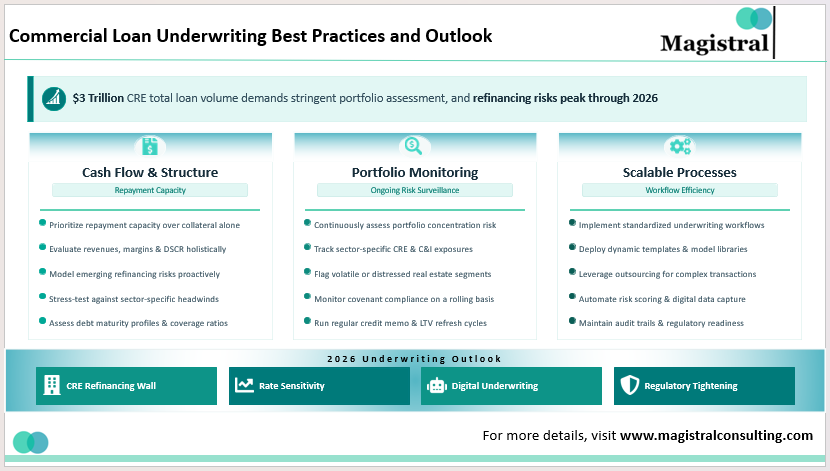

Commercial Loan Underwriting Best Practices and Outlook

Lenders need to balance three factors when underwriting commercial loans because their underwriting process will succeed at its highest level. Institutions require structured processes that enable them to manage increasing demand while maintaining their service quality.

Commercial Loan Underwriting Best Practices and Outlook

Focus on cash flow and structure

Underwriters use repayment capacity as their primary factor to make their lending decisions. Lenders need to evaluate their revenues and margins together with their refinancing risk, while they should not depend solely on their collateral strength.

Portfolio level monitoring

U.S. commercial real estate lenders need to assess their portfolio concentration together with their sector exposure because their total loan volume has surpassed $3 trillion.

Scalable and efficient processes

The establishment of standardized workflows together with templates and outsourcing support enables lenders to achieve efficient underwriting operations. The process becomes especially important when organizations deal with complex transactions that involve private equity and venture capital financing for their borrowers.

How Magistral Supports Commercial Loan Underwriting

Magistral Consulting supports lenders by combining financial expertise with scalable execution capabilities. Their teams assist in financial analysis, credit memo preparation, covenant tracking, and portfolio monitoring, allowing lenders to focus on core decision-making.

They also provide specialized support in areas like cash flow modeling, borrower risk profiling, and collateral analysis, which improves underwriting accuracy and turnaround time. In addition, Magistral’s experience across sectors such as real estate, structured finance, and mid-market lending enables lenders to handle complex transactions more effectively.

Magistral enables institutions to optimize their commercial loan underwriting processes through its combination of technology-based workflows and expert knowledge, which results in cost savings and preservation of high credit quality standards in competitive lending markets.

About Magistral Consulting

Magistral Consulting has helped multiple funds and companies in outsourcing operations activities. It has service offerings for Private Equity, Venture Capital, Family Offices, Investment Banks, Asset Managers, Hedge Funds, Financial Consultants, Real Estate, REITs, RE funds, Corporates, and Portfolio companies. Its functional expertise is around Deal origination, Deal Execution, Due Diligence, Financial Modelling, Portfolio Management, and Equity Research

For setting up an appointment with a Magistral representative visit www.magistralconsulting.com/contact

About the Author

Nitin is a Partner and Co-Founder at Magistral Consulting. He is a Stanford Seed MBA (Marketing) and electronics engineer with 19 + years at S&P Global and Evalueserve, leading research, analytics, and inside‑sales teams. An investment‑ and financial‑research specialist, he has delivered due‑diligence, fund‑administration, and market‑entry projects for clients worldwide. He now shapes Magistral Consulting’s strategic direction, oversees global operations, and drives business‑development support.