The IPO market is undergoing cautious optimism against the prevailing global economic uncertainty, volatile interest rates, and geopolitical tensions. Though investor sentiments have picked up pace from recent times, business houses today are approaching public floats with more emphasis on profitability, sound fundamentals, and sustainable long-term growth opportunities. The IPO market has moved away from early-stage, high-growth startups that incur losses to more established, revenue-focused companies. Equity Research and Analysis is critical in this setting by assisting investors in determining the real value and risk profile of IPO prospects, thus shaping demand and pricing. Institutional investors continue to be discerning, propelling demand for quality issues, while retail participation keeps expanding, spurred by heightened financial literacy and online investment platforms. Consequently, IPO activity is slowly picking up, albeit with companies carefully timing their entrances to coincide with good market windows and investor demand.

Thank you for reading this post, don't forget to subscribe!Fintech Firms Drive the Next Wave of Financial Services IPOs

Fintech companies, such as neo-banks, robo-advisors, and online lenders, lead the IPO pipeline, riding the tidal wave of tech-driven innovation washing over the financial services industry. These firms are transforming the old-style bank and investing by providing cutting-edge, digital-centric solutions that appeal to a younger, more digitally native customer base and underpenetrated markets. Benefitting from equity research and analysis and with their power to grow speedily, bring down operating expenditures, and avail themselves of the power of analytics to create differentiated financial products and services, FinTech IPOs are witnessing substantial investor demand. They have on offer recurring monetization models, customer-driven interfaces, and an ability to remodel financial experiences. Yet, long-term profitability, regulatory resilience, and capacity for growth amid expanding competition will all be crucial when it comes to ensuring enduring prosperity after an IPO.

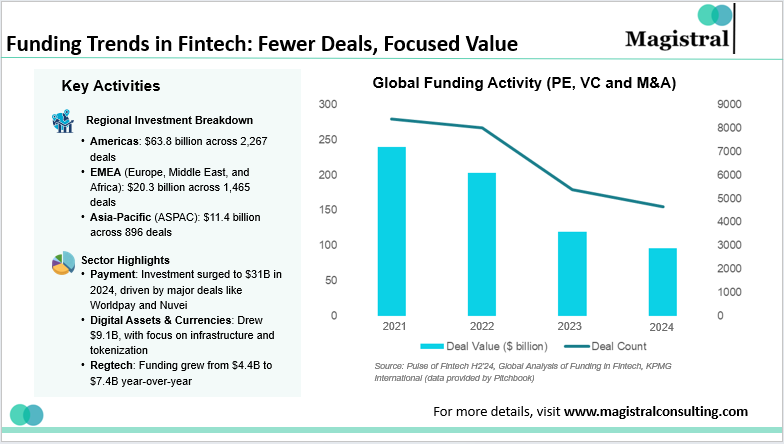

Funding Trends in Fintech: Fewer Deals, Focused Value

Rise of Neo-Banks and Their Public Market Potential

Neo-banks, or digital-only banks, have been successful by providing smooth, app-based banking services without the cost of brick-and-mortar branches. User-centric services, minimal fees, and instant services resonate especially with the youth. While they expand their base of customers and widen offerings, most are making IPO plans to access capital, go international, and cement brand presence. Equity research and analysis are essential to assess the financial performance, business models, and growth opportunities of these neo-banks and make informed investment decisions as these banks go public.

Robo-Advisors Redefining Wealth Management

Robo-advisory platforms use advanced algorithms and data-driven models to provide automated, low-cost investment solutions, enabling wealth management to reach a wider range of retail investors. Through reduced human interaction and tailored portfolio suggestions, the platforms appeal to cost-sensitive consumers looking for effective financial planning instruments. Their technology-driven, scalable business models and recurring advisory fee revenues make them strong candidates for public offerings. As they build out capabilities—with the addition of AI, behavioral finance, and sophisticated data analytics—equity research and analysis are crucial to determining their long-term profitability, competitive positioning, and valuation prior to possible IPOs.

Digital Lending Platforms and Credit Innovation

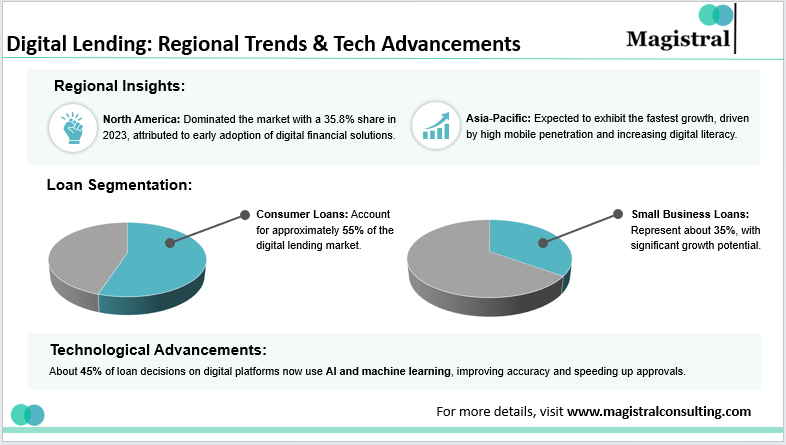

Fintech lenders have dramatically transformed the credit market with fast, analytics-based loan approvals and adaptable financial products. Leverage alternative credit scoring models—examining cash flow, utility bills, and social media data—to cater efficiently to thin-file or underbanked clients commonly neglected by conventional banks.

Digital Lending: Regional Trends & Tech Advancements

As these online lenders scale and expand into new geographies, they are increasingly considered top IPO prospects. But there are challenges ahead, including changing regulatory environments, increasing interest rates, and credit default risk, especially in emerging markets. In this regard, equity research and analysis are essential to assess their risk-adjusted returns, balance sheet quality, loan portfolio quality, and revenue sustainability. Investors use this deep analysis to estimate the long-term sustainability and valuation of digital lenders before possible public listings.

Investor Appetite for Fintech IPOs

Even with wider market uncertainty, FinTech companies remain attractive to investors because of their innovation, scalability, and potential to disrupt traditional financial institutions. In 2024, equity research and analysis revealed that international fintech investment totaled $95.6 billion, down from earlier years but recovering with $25.9 billion raised in Q4 alone, indicating a good year ahead for 2025 (KPMG Pulse of Fintech).

Institutional investors are growingly interested in FinTech businesses that have strong fundamentals, including low customer acquisition costs (CAC)—usually less than $100 per user for top digital players—high lifetime value (LTV), often above $1,000, and gross margins of 60–80%. These are the key signals given by equity research and analysis for long-term profitability and sustainability in the market. Within this setting, equity analysis and research are the key drivers to determine high-potential fintech companies.

In this environment, equity research and analysis play a central role in identifying high-potential fintech firms. By means of detailed financial modeling, benchmarking, and qualitative evaluation, analysts assess not only growth prospects and unit economics but also regulatory risk, market differentiation, and scalability. This allows institutional investors to make well-informed decisions, especially as increasing numbers of FinTechs get ready for IPOs or subsequent rounds of funding in 2025.

Regulatory Landscape and Compliance Challenges

As FinTechs look to go public, they are increasingly subject to regulatory oversight in data privacy, cybersecurity, lending behavior, and capital reserves. In 2024, CFPB’s new regulations under Section 1033 of the Dodd-Frank Act, combined with increasing global cybersecurity threats, compelled financial institutions to invest more in security—estimated to grow to $212 billion by 2025. These regulatory trends require FinTechs to show robust compliance infrastructure and risk management processes to reassure investors.

In this changing environment, equity research and analysis are critical in assessing the readiness of a fintech for public listing. The analysts review regulatory compliance, operational strength, and financial stability—looking at critical measures such as capital buffers, risk exposure, and governance standards. This thorough analysis not only guides institutional investment decisions but also assists in selecting FinTechs that are best poised to thrive in a tighter regulatory environment.

Revenue Models and Profitability Concerns

As fintech businesses move from “growth-at-all-costs” models to more long-term models, pressure increases to prove there are evident roadmaps to profitability. Global fintech revenues in 2024 rose 14% while average EBITDA margins improved 9 percentage points in leading firms, pointing to the turn toward operating efficiency (BCG, 2024). Monzo, for instance, reported its first ever pre-tax profit of £15.4 million, from a £116.3 million loss the year before, led primarily by a 167% jump in net interest income. Revolut, on the other hand, is venturing into ad-based revenue channels, aiming for £300 million in 2026 as part of its drive to diversify (FT, 2024).

Within this context, equity research and analysis are essential in identifying which fintech companies are well-placed for long-term success in public markets. Analysts consider a variety of metrics such as CAC-to-LTV ratios, gross margins, and revenue concentration, as well as reviewing financial transparency, governance practices, and cost control measures. These observations allow institutional investors to spot robust, well-run fintechs with the fundamentals to succeed in the face of growing scrutiny and changing market expectations.

Future Outlook: What’s Next for Fintech in Public Markets

While FinTechs grow out of aggressive expansion measures, profitability, robustness, and prudent operations are now of key interest. In 2024, the industry registered a 14% increase in global revenues, with the leading players experiencing EBITDA margin gains of up to 9 percentage points (BCG, 2024). Monzo registered its first ever pre-tax profit of £15.4 million, overturning a dramatic loss the previous year, mainly on the back of a 167% jump in net interest income. Revolut, on the other hand, is hoping to reach £300 million of ad revenue by 2026 as it looks to diversify revenues and lessen reliance on transactional fees (FT, 2024).

Against this backdrop, equity research and analysis form critical tools in evaluating IPO-readiness and investment potential in the long term. Analysts assess operational efficiency based on metrics such as CAC-to-LTV ratios, subscription-based revenue models, and trends in margins. Equally crucial, they test corporate governance, regulatory compliance, and transparency—critical drivers to winning investor confidence as fintechs prepare for listing in the public markets.

About Magistral Consulting

Magistral Consulting has helped multiple funds and companies in outsourcing operations activities. It has service offerings for Private Equity, Venture Capital, Family Offices, Investment Banks, Asset Managers, Hedge Funds, Financial Consultants, Real Estate, REITs, RE funds, Corporates, and Portfolio companies. Its functional expertise is around Deal origination, Deal Execution, Due Diligence, Financial Modelling, Portfolio Management, and Equity Research

For setting up an appointment with a Magistral representative visit www.magistralconsulting.com/contact

About the Author

The article is authored by the Marketing Department of Magistral Consulting. For any business inquiries, you can reach out to prabhash.choudhary@magistralconsulting.com

[sp_easyaccordion id=”3646″]